Vacation rental property tax rules can make or break your investment returns. The IRS treats these properties differently than regular rentals, with specific classifications that directly impact your tax liability.

We at Up North Property Management see property owners lose thousands annually by misunderstanding these regulations. Getting the tax strategy right from day one protects your profits and keeps you compliant with federal requirements.

How Does the IRS Classify Your Vacation Rental?

The IRS uses three distinct classifications for vacation rental properties, and your classification determines everything from allowable deductions to tax reporting requirements. Properties rented fewer than 15 days annually fall under the 14-day rule, where rental income remains tax-free but no rental expenses can be deducted. This classification works best for high-value properties in premium locations where short-term rental rates exceed $500 per night.

Personal Use vs Rental Use Calculations

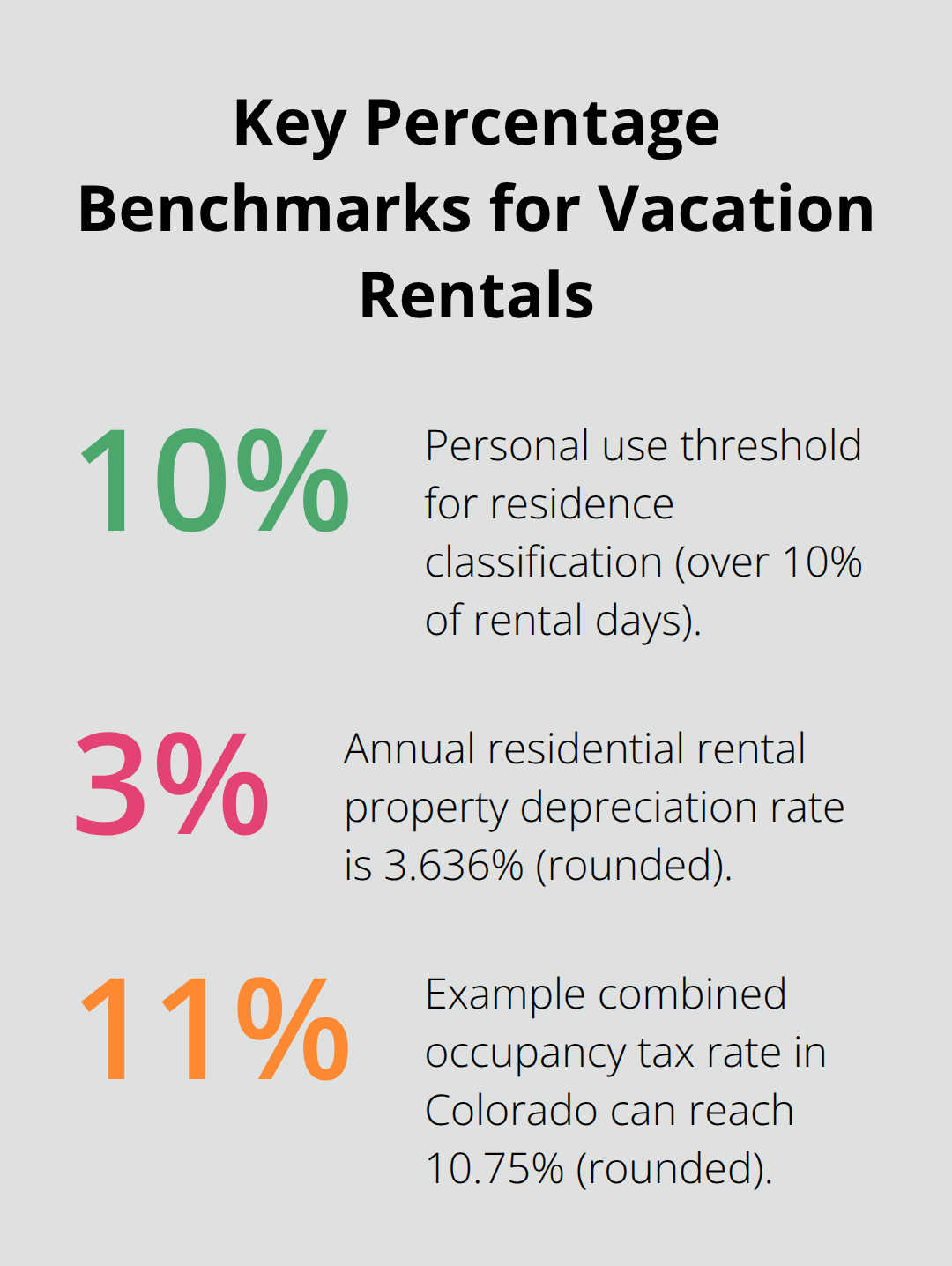

Your property becomes a residence for tax purposes when personal use exceeds either 14 days or 10% of total rental days at fair market value. Personal use includes any time you, family members, or friends use the property without payment of fair rental rates. The IRS counts maintenance and repair time as business use, not personal use (which many owners overlook). Properties classified as residences face the rental income limitation rule, where deductible expenses cannot exceed rental income for the year.

Investment Property vs Business Operation Status

Properties rented 15 days or more with minimal personal use qualify as investment properties, which allows rental losses to offset other income subject to passive activity loss rules. The IRS treats properties that provide substantial services like daily housekeeping or meal service as business operations that require Schedule C reports instead of Schedule E. Investment property status offers significant tax advantages, including depreciation deductions and the ability to deduct expenses that exceed rental income.

Mixed-Use Property Calculations

Properties with both personal and rental use require expense proration based on rental days divided by total days used. The IRS requires owners to track rental days (days rented at fair market value) separately from personal use days. This calculation method affects which expenses you can deduct and how much rental income you must report (particularly important for properties used frequently by owners).

The specific expenses you can write off depend entirely on your property classification, which leads directly into the types of deductions available for each category.

Which Expenses Can You Deduct From Rental Income

Vacation rental expense deductions can reduce your tax liability when owners apply them correctly. The IRS allows property owners to deduct ordinary and necessary expenses that relate directly to rental operations, but the specific expenses depend on your property classification. Properties that the IRS classifies as residences face the rental income limitation where total deductions cannot exceed gross rental income for the year, while investment properties allow unlimited deductions subject to passive activity loss rules.

Operating Expenses That Reduce Your Tax Bill

Mortgage interest represents the largest deduction for most vacation rental owners and often accounts for 60-80% of total deductible expenses according to IRS data. Property taxes, insurance premiums, utilities, and management fees qualify as fully deductible expenses that reduce taxable income. Advertising costs include platform fees from Airbnb or VRBO, professional photography, and website maintenance that reduce your taxable income dollar-for-dollar.

Repairs that maintain property condition like appliance fixes, paint jobs, or plumbing work qualify as current-year deductions. Improvements that add value must be depreciated over 27.5 years instead. Legal and professional fees for tax preparation, property management contracts, and tenant disputes count as deductible business expenses (many owners overlook these completely).

Depreciation Deductions for Rental Properties

Residential rental properties qualify for depreciation deductions worth 3.636% of the property’s basis annually over 27.5 years. This depreciation can generate $2,000-5,000 in annual tax savings for typical vacation rentals. The IRS requires owners to claim depreciation whether they take the deduction or not, which affects the property’s basis when sold.

Home Office and Travel Expense Benefits

Home office deductions apply when you use part of your primary residence exclusively for rental property management. The IRS offers two calculation methods: the simplified method at $5 per square foot up to 300 square feet, or the actual expense method based on the percentage of home used for business purposes.

Travel expenses to inspect, maintain, or manage your rental property qualify for full deduction. This includes mileage at 65.5 cents per mile for 2023, plus lodging and meals when trips require overnight stays (the IRS requires overnight travel for meal deductions).

These deduction strategies work hand-in-hand with proper tax reporting, which requires specific forms and documentation to satisfy IRS requirements.

What Forms Must You File for Vacation Rental Taxes

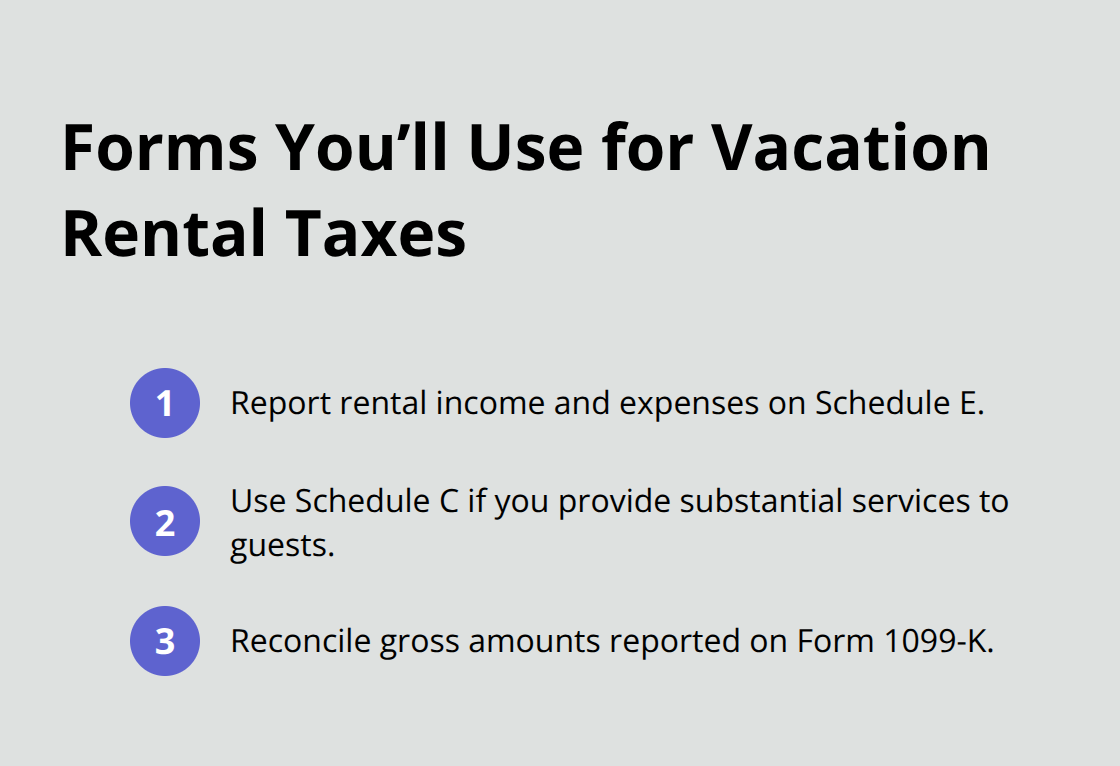

Vacation rental tax reports require specific forms that vary based on your rental income and property classification. Schedule E serves as the primary form for most vacation rental owners, where you report rental income on line 3 and deduct allowable expenses like mortgage interest, property taxes, depreciation, and costs. The IRS requires Schedule E when your property generates rental income for 15 days or more annually, and this form calculates your net rental profit or loss that flows to your Form 1040. Properties that provide substantial services like daily housekeeping must use Schedule C instead, which treats the operation as an active business rather than passive rental income.

Payment Processor Reports Change Everything

Form 1099-K reports payments from payment apps or online marketplaces and from credit, debit or stored-value cards. Payment processors like Airbnb, VRBO, and PayPal now issue 1099-K forms for qualifying transactions, which reports gross rental income including taxes, fees, and cleaning charges collected on behalf of guests. The 1099-K amount will exceed your actual rental income because it includes non-rental items, so you must reconcile the difference on Schedule E and subtract taxes and fees collected for third parties. Payment processors send these forms by January 31st, and the IRS receives copies automatically.

State and Local Tax Complexity Demands Attention

Most states impose occupancy taxes that range from 3% to 14% on short-term rentals, with popular vacation destinations like Colorado that charge up to 10.75% combined state and local rates. States classify vacation rentals differently for property tax purposes, with 19 states that lack specific short-term rental classifications and others that treat them as commercial properties with higher tax rates. Local municipalities often layer additional taxes and license requirements, which creates compliance obligations that vary dramatically between jurisdictions. Wisconsin requires vacation rental operators to register for sales tax permits and collect state taxes, while Minnesota imposes both state and local taxes that must be remitted monthly when collections exceed specific thresholds.

Final Thoughts

Vacation rental property tax rules demand strategic action to maximize your investment returns. You must track personal versus rental use days with precision, as this single calculation determines your entire tax treatment and available deductions. Set up separate bank accounts for rental income and expenses to simplify record-keeping and avoid personal fund complications.

Property owners lose thousands annually when they fail to claim depreciation deductions. Many also misclassify repairs as improvements and miss immediate tax benefits. Never assume the 1099-K amount equals your taxable income, as it includes taxes and fees collected for third parties that you must subtract.

Professional tax guidance becomes necessary when your rental generates significant income or operates across multiple states. Up North Property Management handles operational complexities while you focus on tax optimization strategies. Plan your tax approach before you purchase rental property, as classification decisions in year one affect your tax liability for the entire ownership period.