Buying a cabin doesn’t require a traditional mortgage. We at Up North Property Management know that many buyers find creative cabin financing solutions work better for their situation.

This guide covers owner financing, personal loans, hard money lenders, and government programs that can help you purchase your cabin.

Owner Financing and Seller Financing Models

Owner financing cuts out the bank entirely. The cabin seller becomes your lender, and you make payments directly to them over an agreed timeframe. This works especially well in rural cabin markets where traditional lenders hesitate to finance properties. Classic Country Land, which has operated since 1999, pioneered this model for land and cabin purchases across multiple states. They require a minimum down payment of $249 and charge a base interest rate of 12.99%, though larger down payments can lower your rate. The entire process happens in-house through a contract for deed, meaning no credit checks, no background investigations, and no discrimination based on credit history. You gain immediate use of the property while repaying the seller, which eliminates months of bank approval delays. The flexibility here matters most-terms adjust to fit your situation rather than forcing you into rigid lending boxes. If you have inconsistent seasonal income from tourism work or agriculture, owner financing evaluates your complete financial picture instead of demanding two years of tax returns that may not reflect your current earning potential.

Speed and Accessibility Advantages

The speed advantage alone changes the game. Traditional mortgages take 30 to 45 days minimum; owner financing closes in weeks. You avoid appraisal requirements, underwriting delays, and the frustration of loan denials based on credit scores or income documentation. Seasonal cabin buyers with irregular deposits find this especially valuable since sellers can structure payments around your actual cash flow patterns. If you plan to rent out the cabin for income, the seller may factor potential rental revenue into the loan terms, which increases your borrowing power. However, interest rates typically run higher than conventional mortgages. A 12.99% rate beats payday lending but costs more than a 6% traditional mortgage over 15 or 30 years. You should calculate the total interest paid before committing.

Understanding the Risks

Seller financing shifts risk onto you as the buyer. If the seller lacks patience or faces financial hardship, they might sell the contract to a debt collector, which complicates your ownership. You must protect yourself through proper documentation. A contract for deed should never be a handshake agreement-it needs to be a formal, written document that both parties sign. This protects your investment and clarifies expectations from day one.

Negotiating Terms That Work for Everyone

Down payments don’t need to be massive. Classic Country Land accepts $249 minimum, which helps buyers with limited capital. You negotiate the full purchase price, interest rate, loan term, and payment schedule directly with the seller. A longer term means lower monthly payments but more total interest; a shorter term costs less overall but strains monthly cash flow. You should build in contingencies for property inspections and title verification before signing anything. Sellers benefit from steady income and avoid realtor commissions, typically 5 to 6% of the sale price. This savings should translate into better terms for you. Work with a real estate attorney to draft the contract for deed properly. This costs $500 to $1,500 but protects both parties and prevents disputes later. The contract should include details about property maintenance responsibilities, insurance requirements, property tax payments, and what happens if either party defaults. Owner financing works best when both buyer and seller understand the terms completely and commit to a transparent process.

With owner financing established as one path forward, personal loans and alternative lenders offer another route for cabin buyers who want to explore additional options beyond seller arrangements.

Personal Loans and Alternative Lending Solutions

Personal loans offer cabin buyers a straightforward alternative when owner financing or traditional mortgages don’t fit. These unsecured loans typically range from $1,000 to $100,000, though larger amounts exist through some lenders. You get approved in days, not weeks, and funds transfer directly to your account with no property appraisal required. Interest rates vary wildly depending on your credit score. Borrowers with excellent credit (750+) might secure rates around 6% to 8%, while those with fair credit face 15% to 25% rates. This matters significantly over time. A $100,000 personal loan at 8% costs roughly $23,000 in interest over ten years; the same loan at 20% costs nearly $65,000. Calculate the total cost and compare it against owner financing or alternative options before pursuing a personal loan.

Hard Money Lenders and Private Investors

Hard money lenders take a different approach entirely. These private investors loan money based primarily on the property’s value, not your credit history or income documentation. They typically lend 60% to 75% of the property’s after-repair value, making them useful for cabin purchases where traditional lenders hesitate. Hard money loans carry steeper costs-interest rates commonly range from 10% to 18%, with origination fees of 2% to 5% added upfront. The tradeoff is accessibility. If you have poor credit or non-traditional income, hard money lenders move forward when banks decline you. Loan terms run shorter than mortgages, typically 12 months to 5 years, which means higher monthly payments but faster ownership. This works well if you plan to refinance into a traditional mortgage once you’ve owned the property for 12 months and established a payment history.

Credit Unions and Community Banks

Credit unions and community banks deserve serious consideration before exploring hard money territory. Credit unions often offer cabin loans at rates 1% to 2% lower than traditional banks, sometimes reaching 5% to 6% for well-qualified borrowers. Community banks typically maintain relationships with local borrowers and understand seasonal income patterns that national lenders dismiss outright. Many community banks in rural areas actively finance cabin purchases because they know the local market and understand that agricultural or tourism income fluctuates predictably. Membership credit unions affiliated with specific employers or geographic regions sometimes offer special cabin financing programs designed for their communities. You speak with actual underwriters who can explain their decision logic rather than automated systems. Credit unions offered competitive rates for cabin purchases, substantially beating hard money lenders.

Comparing Your Options

Contact three to five local credit unions and community banks within 50 miles of the cabin property. Ask specifically about second-home financing and whether they’ve financed similar properties in that area. Request their best rate for borrowers with your credit profile. Compare the total cost across all options-owner financing, personal loans, hard money, and credit unions-because the difference between a 7% rate and a 15% rate amounts to tens of thousands of dollars over the loan term. The cheapest option isn’t always best if it requires a longer approval period that risks losing the property to another buyer, but don’t overpay simply because you’re impatient. With personal loans and private lenders evaluated, government programs and grants present another avenue worth exploring for cabin buyers seeking additional financial support.

Government Programs and Grants for Cabin Owners

USDA Rural Development loans represent the strongest government option for cabin buyers in rural areas, though the program carries restrictions most people overlook. The USDA targets properties in eligible rural zones, which excludes suburbs and areas near major cities. If your cabin qualifies geographically, you access loans with down payments as low as 3% and interest rates competitive with conventional mortgages, sometimes 0.5% to 1% lower. The catch: the property must serve as your primary residence, not a vacation retreat or rental investment. This disqualifies most cabin buyers outright, making USDA loans less practical than they initially appear. Contact your local USDA office to confirm whether your cabin property falls within an eligible rural area before investing time in the application. The process takes 45 to 60 days, longer than owner financing but faster than traditional mortgages.

State and Local Tax Incentives

State and local incentive programs vary dramatically by location, so a generic approach fails here. Some states offer property tax breaks for conservation easements if you preserve land or protect forests on your cabin property. Minnesota provides tax incentives for sustainable forestry practices on residential land. Wisconsin offers agricultural property tax exemptions that occasionally extend to rural cabins used partially for agricultural purposes. These programs rarely fund cabin purchases directly but reduce your ongoing ownership costs significantly. Research your specific state’s department of natural resources and revenue websites to identify available programs. Many states hide these incentives in obscure corners of their websites, so calling the office directly often proves faster than searching online. Local county assessors can point you toward applicable programs in your specific jurisdiction.

Rental Property Tax Deductions

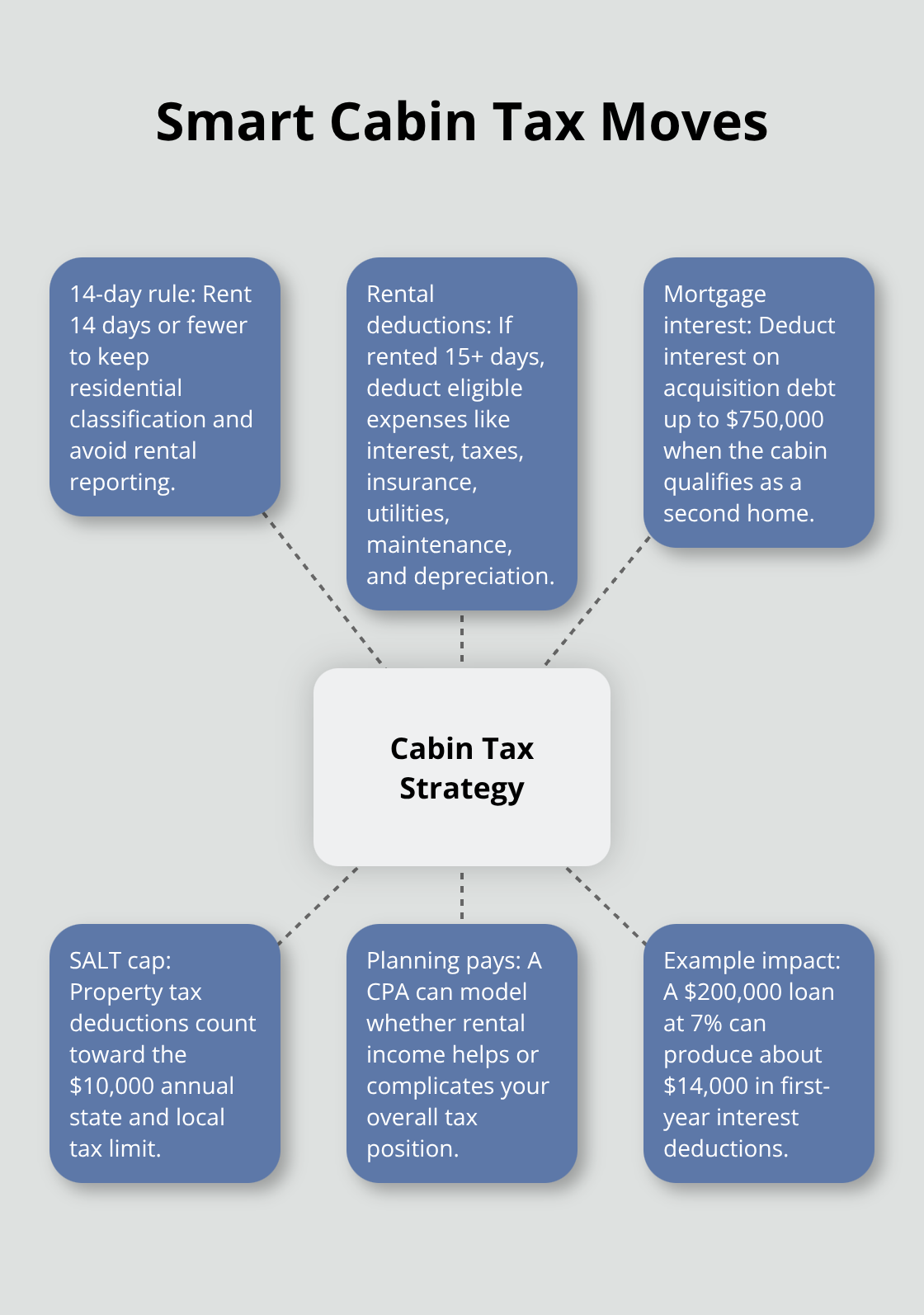

Tax deductions for cabin owners matter far more than most people realize, especially if you rent the property part-time. The IRS allows rental deductions for cabins rented to others, including mortgage interest, property taxes, insurance, utilities, maintenance, and depreciation. If you rent your cabin 14 days or fewer annually, the property maintains residential classification and you avoid rental property complications. Rent it 15 or more days per year and you shift into investment property territory, which opens deductions but triggers additional tax reporting requirements. Many cabin owners structure their usage strategically around this 14-day threshold to optimize tax benefits while avoiding the administrative burden of investment property status.

Strategic Tax Planning for Cabin Ownership

A CPA familiar with vacation property taxation can model your specific scenario and identify whether rental income actually benefits you or creates unnecessary tax complications. The math often surprises cabin owners who assume rental income automatically improves their financial position. Mortgage interest deductions on your cabin remain available if the property qualifies as a second home under IRS guidelines, allowing you to deduct interest on loans up to $750,000 in acquisition debt. Property tax deductions apply regardless of whether you rent the cabin, subject to the $10,000 annual limitation on state and local taxes. These deductions compound over decades of ownership. A cabin financed with a $200,000 loan at 7% generates roughly $14,000 in first-year interest deductions alone.

Over 15 years, that compounds into substantial tax savings. Consult a tax professional before purchasing to understand how cabin ownership affects your overall tax situation rather than discovering surprises at filing time.

Final Thoughts

You now have five distinct paths to cabin ownership beyond traditional mortgages. Owner financing offers speed and flexibility when sellers work with you directly, personal loans and hard money lenders provide quick capital if you have limited time or non-traditional income, and credit unions often beat national lenders on rates. Government programs like USDA Rural Development loans work for primary residences in eligible rural areas, while tax deductions and strategic rental income planning substantially reduce your long-term ownership costs.

The right cabin financing option depends entirely on your situation. If you have poor credit or seasonal income, owner financing through companies like Classic Country Land eliminates credit checks and evaluates your complete financial picture. If you need speed and have equity elsewhere, a personal loan closes in days, and if you’re in a rural area planning to live there full-time, USDA loans offer competitive rates. Contact three to five potential lenders representing different approaches, request quotes, and compare total costs over your intended loan term rather than focusing solely on interest rates.

Once you own your cabin, consider working with Up North Property Management if you’re in Northern Minnesota-they handle marketing, bookings, cleaning, and maintenance for vacation rentals, transforming your cabin into a revenue-generating asset while you avoid operational headaches. This rental income can offset your financing costs and accelerate your path to building equity. Evaluate these cabin financing alternatives honestly, run the numbers carefully, and move forward with the option that fits your financial reality and timeline.