Swapping a rental property for a vacation home through a 1031 exchange can save you thousands in taxes while repositioning your real estate portfolio. The process has strict rules and tight deadlines, but it’s entirely manageable when you know what to expect.

We at Up North Property Management have guided property owners through this transition countless times. This guide walks you through each step, from finding the right replacement property to avoiding costly mistakes.

What Makes a Property Eligible for Exchange

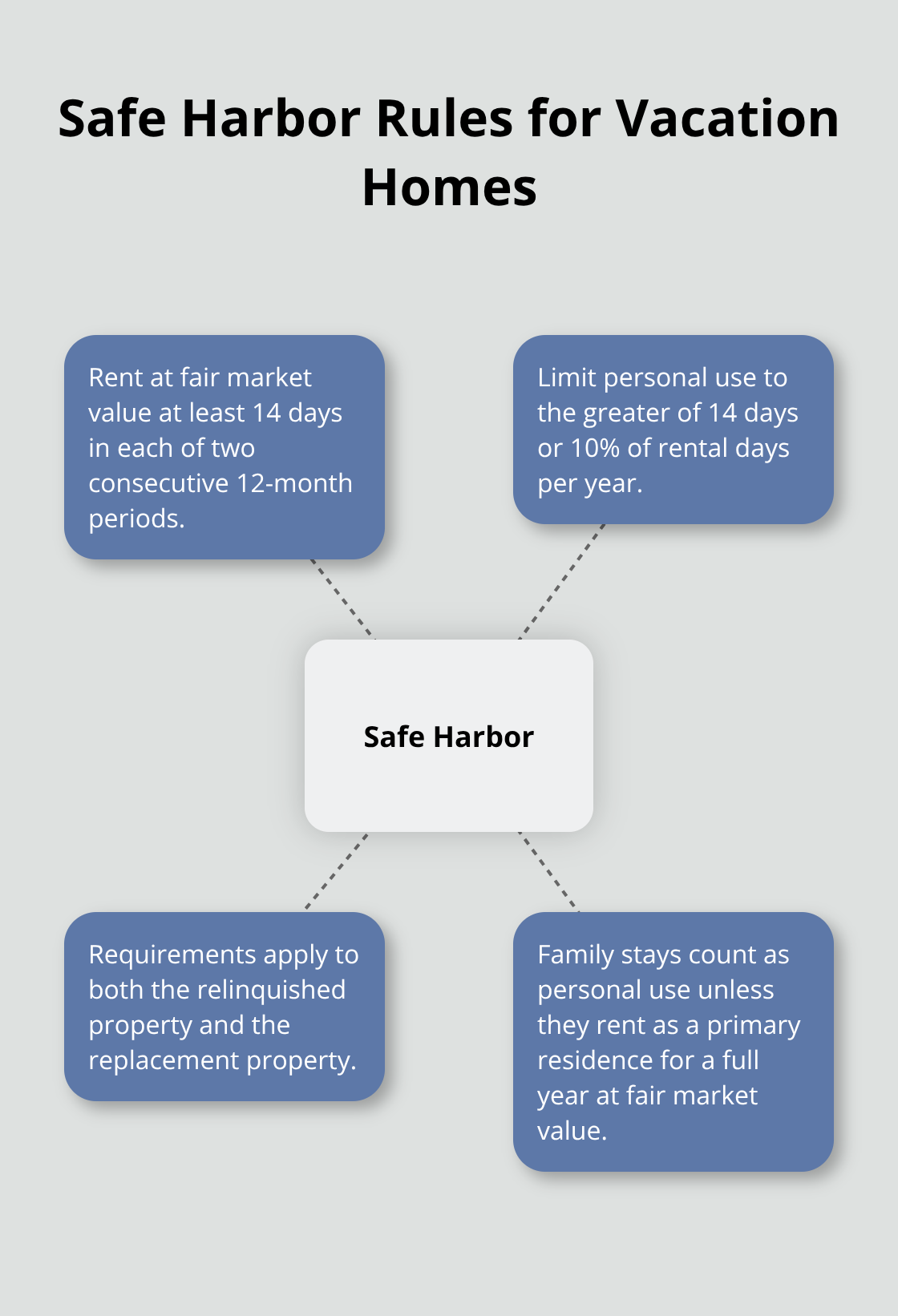

A 1031 exchange treats rental properties and vacation homes as like-kind assets under IRS rules, so you can swap one for the other without triggering immediate capital gains taxes. The IRS considers real property held for investment or business use as like-kind, regardless of whether you exchange a long-term rental for a vacation home or vice versa. What matters is investment intent, not the specific property type. However, the IRS draws a hard line between investment properties and personal residences. If your vacation home serves primarily for personal enjoyment rather than rental income, the IRS will not permit a 1031 exchange. Under IRS Revenue Procedure 2008-16, vacation homes qualify only if you rent them at fair market value for at least 14 days in each of two consecutive 12-month periods while limiting personal use to the greater of 14 days or 10% of rental days per year. This safe harbor proves investment intent and applies both to the property you sell and the replacement you acquire.

The 24-Month Ownership Window

Before you exchange into a vacation home, you must own your current rental property for at least 24 months immediately preceding the sale. This 24-month period consists of two consecutive 12-month periods, and in each period, the property must be rented for at least 14 days at fair market value. Personal use cannot exceed the greater of 14 days or 10% of the days you rented the property. If you rented a property 140 days in a year, you cap out at 14 days of personal use since 10% of 140 equals only 14 days. Renting to family members counts as personal use unless they rent the property as a primary residence for a full year at fair market value. Many owners lose exchange eligibility by allowing relatives to stay for free or at discounted rates. After the exchange closes, the same rules apply to your replacement vacation home for another 24 months. You cannot skip this requirement or shorten it.

The 45-Day and 180-Day Deadlines

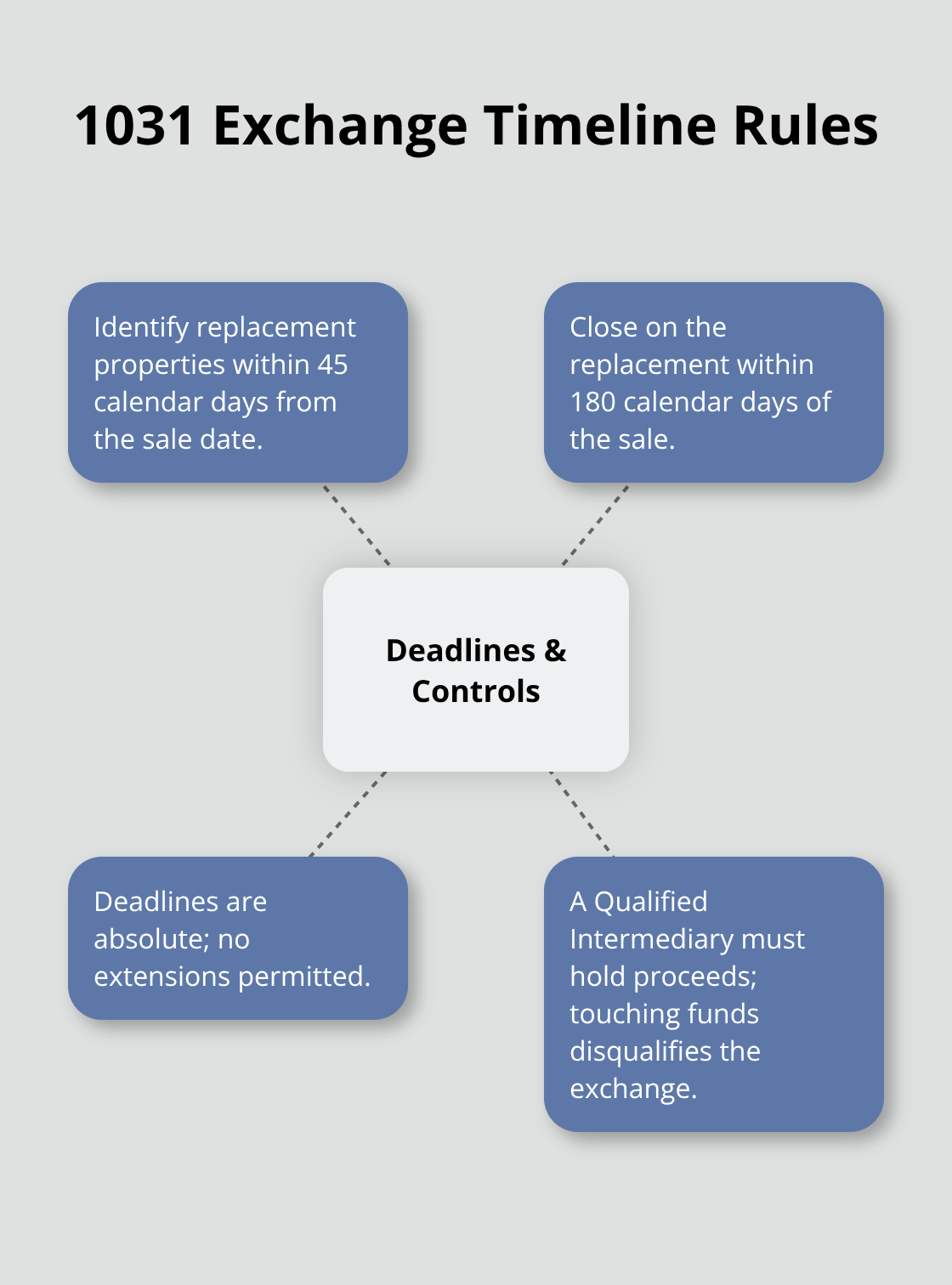

The IRS imposes two non-negotiable deadlines once you sell your rental property. You have 45 calendar days to identify one or more replacement properties and 180 calendar days from the sale date to close on the replacement. These deadlines are absolute and cannot be extended. A Qualified Intermediary must hold your sale proceeds during this period; you cannot touch the money yourself or the exchange fails.

Missing even one deadline disqualifies the entire transaction and triggers full capital gains tax liability.

Tax Deferral Impact and Property Valuation

The tax deferral benefit is substantial. A 1031 exchange defers federal and state capital gains taxes and depreciation recapture. If you sold a rental property for $500,000 with a $300,000 gain, deferring that gain could save you significant taxes in combined federal and state liability. That deferred amount stays invested in your replacement property, compounding your real estate wealth over time. The catch is that both the relinquished and replacement properties must be valued equally or the replacement must be worth more to preserve full tax deferral. If you exchange into a cheaper property, you owe taxes on the difference. Understanding these valuation rules prevents costly mistakes as you move forward with identifying your replacement vacation home.

Making Your Exchange Happen

Securing a Qualified Intermediary

The IRS requires a Qualified Intermediary to hold your sale proceeds and facilitate the entire transaction-this is not optional. Atlas 1031 Exchange, LLC is one example of a QI that specializes in these arrangements. The intermediary cannot be you, your real estate agent, your accountant, or anyone with a financial interest in the transaction. This person or company acts as a neutral third party, holding funds between the sale and purchase. Many owners attempt to manage the process themselves, which is a critical mistake. The moment you touch the proceeds from your rental property sale, the exchange fails and you owe full capital gains taxes. Your QI will provide detailed instructions on wire transfers and timelines. Start vetting intermediaries at least two weeks before listing your rental property so you can move quickly once an offer arrives. Most QIs charge between $500 and $1,500 depending on transaction complexity.

Identifying Replacement Properties Within 45 Days

The 45-day identification window begins the moment your sale closes, not when you sign the contract. This compressed timeline forces you to act decisively. You can identify up to three properties under the three-property rule, or use the 200% rule to identify unlimited properties as long as their combined value does not exceed 200% of your relinquished property’s value. If your rental sold for $400,000, you can identify properties totaling up to $800,000. The identification must be in writing to your QI before midnight on day 45. Many owners waste time analyzing properties they ultimately cannot afford or do not want, burning through their window. You need a pre-approved financing strategy before day 1 to move fast once you identify a target.

Meeting the 180-Day Closing Deadline

The 180-day deadline is equally rigid-you must close on your replacement vacation home by day 180 from the sale date. This means scheduling inspections, appraisals, and underwriting within a compressed timeframe. Working with a lender experienced in 1031 exchanges eliminates delays since they understand the urgency and can expedite approvals. Closing day 179 counts as compliant; closing day 181 disqualifies the entire exchange. Your QI will send you a checklist of required documents and signatures.

Verifying Safe Harbor Compliance Before Closing

The replacement property must meet the safe harbor rental requirements covered earlier. Properties in high-demand vacation markets with strong seasonal rental activity make this requirement easier to satisfy. If you plan to hire a property manager to handle bookings and tenant relations, confirm their experience with vacation rental compliance and documentation. The next section covers the mistakes that derail exchanges even when owners follow the basic steps correctly.

Common Mistakes That Derail 1031 Exchanges

The 45-day and 180-day deadlines exist for a reason-they weed out unprepared exchanges that collapse under pressure. One day past the deadline triggers immediate tax liability on your entire gain, and the IRS does not grant extensions. Owners lose six-figure tax deferrals because they misjudge how long financing takes or underestimate the complexity of identifying a suitable vacation property. The deadline pressure demands action before you sell your rental.

Start Your Preparation Two Months Early

Contact your Qualified Intermediary and lender at least 60 days before listing your property. Many owners wait until after the sale closes to begin these conversations, which is backwards. Your QI needs to understand your timeline and target replacement property type in advance so they can prepare documentation templates and coordinate with title companies. If you delay this preparation, you will spend your 45-day window scrambling instead of strategically evaluating properties.

One practical step that saves weeks is pre-identifying your target vacation market before the sale closes. Research seasonal rental demand, average nightly rates, and property management availability in areas where you want to own. This groundwork lets you move decisively once the 45-day clock starts ticking.

Budget for Hidden Costs Before You List

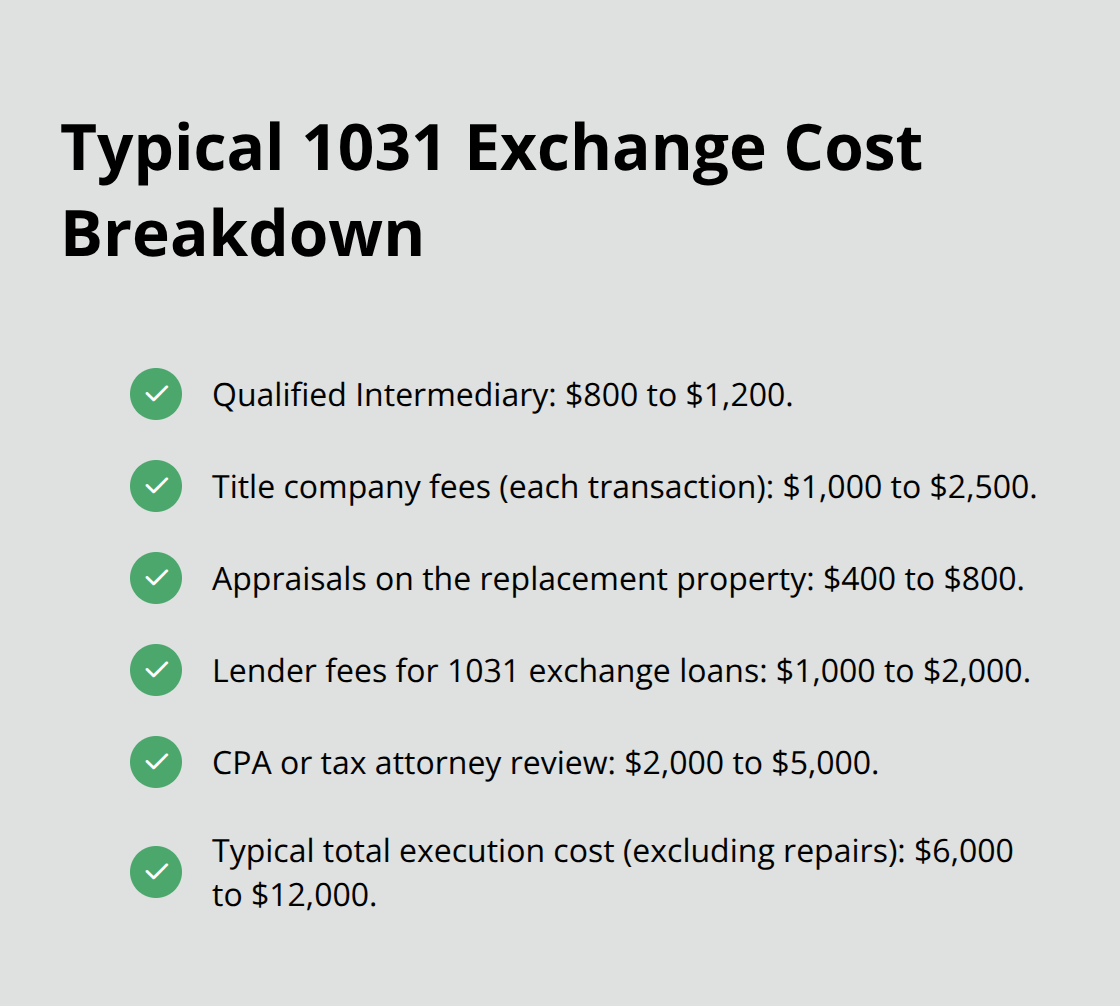

Underestimating the true cost of a 1031 exchange catches owners off guard. Your Qualified Intermediary charges between $800 and $1,200, but that is only the beginning. Title company fees for both the sale and purchase typically run $1,000 to $2,500 per transaction. Appraisals on the replacement property to verify equal or greater value add another $400 to $800.

Lenders originating a 1031 exchange loan often charge slightly higher fees than conventional mortgages because the underwriting is more complex and time-sensitive. Budget an additional $1,000 to $2,000 in lender fees. Inspections, surveys, and any required repairs discovered during due diligence add unpredictability to your costs. Many owners also hire a CPA or tax attorney to review the exchange structure and confirm safe harbor compliance on the vacation home side, which costs $2,000 to $5,000 depending on complexity.

The total cost of executing a 1031 exchange typically runs $6,000 to $12,000, not including any property repairs or upgrades needed on the replacement vacation home. Failing to budget for these costs forces owners to touch their sale proceeds or reduce the replacement property’s purchase price, both of which damage the tax deferral or trigger partial tax liability. Calculate your total exchange costs before you list your rental property and factor them into your replacement property budget so you do not compromise your investment thesis mid-transaction.

Final Thoughts

A 1031 exchange from rental property to vacation home succeeds when you plan ahead, respect the deadlines, and budget for the full cost of execution. The tax deferral is real and substantial, but only if you follow the IRS rules precisely. Missing a single deadline or touching your sale proceeds derails the entire transaction and triggers immediate capital gains tax liability.

The safe harbor requirements for vacation homes demand consistent rental activity and documented personal use limits across a four-year window. This is not a burden if you plan to actively rent your replacement property and generate income. Many owners discover that vacation rental income offsets their mortgage and property costs, turning the exchange into a wealth-building move rather than a tax-deferral exercise alone.

Vacation rental management is where most owners stumble after closing the exchange. You can own the perfect property in a high-demand market, but poor marketing, inconsistent bookings, and maintenance neglect kill your rental income and jeopardize safe harbor compliance. If your replacement property is in Northern Minnesota, Up North Property Management handles the operational side so you do not have to.