Lakefront properties attract investors for good reason-they command premium prices and generate strong rental income. We at Up North Property Management have seen firsthand how the right lakefront investment can outperform traditional residential properties.

But buying lakefront real estate requires more than just finding a beautiful view. You need to understand water quality, local regulations, market trends, and the financial realities that separate profitable investments from costly mistakes.

Where Should You Buy? Analyzing Location Before You Invest

Water Quality Sets the Foundation

Water quality determines everything about a lakefront property’s appeal and long-term value. Spring-fed lakes typically maintain clearer water and more stable ecosystems than dam-controlled lakes, which experience significant seasonal level fluctuations that can damage docks and shorelines. Test the water yourself before committing capital-pH levels, clarity, and algae presence directly affect both rental demand and your maintenance costs. A simple water quality test from a county lab costs under $100 and reveals whether swimmers will actually use the property or if you’re stuck marketing a murky investment.

Dock Depth and Water Access Matter

Accessibility shapes your rental market more than most investors realize. Properties on all-sports lakes command higher rental rates because they attract boaters, but they also bring noise and traffic that some guests reject. No-wake lakes offer tranquility but limit motorized recreation. Verify dock depth too-shallow docks under four feet cannot accommodate most boats, which eliminates an entire rental market segment. According to Statista, about 40% of waterfront property buyers rank proximity to water access as a top search criterion, but that access means nothing if the water cannot support their intended activities.

Economic Growth Signals Stronger Returns

Tourism trends in your target region directly predict rental occupancy and pricing power. Research whether the area experiences job growth, new attractions, or infrastructure improvements. Counties with rising employment and new recreational amenities see faster property appreciation and higher nightly rental rates. Lake McQueeney in Central Texas, for example, experiences concentrated summer demand when families vacation, allowing owners to charge premium rates during peak weeks. Conversely, lakes near declining towns struggle to fill vacancies year-round, crushing cash flow projections. Check local economic reports, chamber of commerce data, and tourism board statistics to confirm whether demand is growing or stagnating.

Seasonal Patterns Drive Your Income

Seasonal patterns vary dramatically by geography and lake type-understanding your specific market’s peak rental window prevents overestimating income. A property that rents for $300 per night in summer but sits vacant eight months annually generates far less revenue than one with steadier shoulder-season demand. Calculate realistic occupancy rates by reviewing what comparable properties actually achieve on platforms like Airbnb and VRBO, not what owners claim they could achieve. Once you understand your market’s seasonal rhythm and economic trajectory, you can assess whether the property itself will hold its value and generate consistent returns.

Property Condition and Long-Term Value

Shoreline Deterioration Costs More Than Most Investors Expect

Shoreline deterioration and structural failures drain lakefront investments faster than poor rental seasons. Hire a professional engineer to inspect both the home’s structural integrity and the shoreline’s stability before you commit capital. Erosion, seawall failure, and foundation damage from water exposure cost $15,000 to $100,000+ to repair, and most standard home inspectors miss these issues entirely. Test soil composition and water table levels to confirm the foundation sits on stable ground. If the property has a dock, verify its condition separately-replacement docks run $10,000 to $40,000 depending on size and materials. Many investors skip this step and inherit someone else’s deferred maintenance.

Water level fluctuations also damage shorelines over time. Spring-fed lakes with stable levels pose less risk than dam-controlled systems where annual fluctuations exceed ten feet. Document the lake’s historical water levels and erosion patterns through county records before closing.

Shoreline Setbacks and Compliance Requirements

Shoreline setback requirements vary by county, and violating them triggers costly remediation orders. Confirm the property complies with local setback laws before purchase, or you may be forced to remove structures or lose rental appeal. Contact the county planning department directly to verify compliance-do not rely on the seller’s assurances. Environmental regulations around septic systems, stormwater management, and shoreline vegetation also constrain what you can modify. If you plan renovations, obtain written confirmation that planned improvements comply with local rules before purchase.

Zoning and Rental Restrictions Shape Your Profit Potential

Permits and zoning restrictions determine whether your investment can actually operate as a rental. Some lakefront communities prohibit short-term rentals entirely, while others cap occupancy or require special licensing that costs hundreds monthly. Confirm whether the property sits in a FEMA flood zone, as flood insurance premiums can exceed $2,000 annually and some lenders refuse to finance properties in high-risk zones.

Research whether your target county welcomes or discourages short-term rentals through planning documents and recent variance approvals. Markets where local governments actively support vacation rentals see stronger investor demand and faster value growth. This regulatory clarity often matters more than square footage or view quality when projecting long-term returns.

How Regulations Drive Regional Appreciation Rates

Property appreciation in lakefront markets depends heavily on regulatory factors. Properties in counties with reasonable permitting timelines and stable zoning appreciate 15% to 25% faster than those in restrictive jurisdictions, according to regional market analyses. The difference between a welcoming regulatory environment and a hostile one can add hundreds of thousands to your property’s value over a decade. Understanding these local rules before purchase separates investors who build wealth from those who struggle with unexpected compliance costs and restrictions that kill rental potential. With shoreline stability confirmed and regulatory requirements mapped out, you can now assess the financial fundamentals that determine whether this property generates the returns you need.

Does Your Lakefront Investment Actually Pencil Out?

Realistic Occupancy Rates Beat Fantasy Projections

Most investors overestimate occupancy by 20% to 40%, assuming properties will book solid during shoulder seasons when comparable properties sit half-empty. Pull actual booking data from Airbnb and VRBO for properties similar to your target, filtering by season and price point using tools like AirDNA. If comparable homes achieve 55% occupancy annually at $250 per night, your property generates roughly $50,000 gross revenue yearly, not the $100,000 some sellers claim. Multiply realistic occupancy rates by your nightly rate, account for platform fees that typically consume 15% to 20% of revenue, then subtract actual costs before celebrating your returns.

Maintenance Costs Destroy Thin Profit Margins

Lakefront properties maintenance costs run substantially higher than inland homes due to weather exposure, dock repairs, and shoreline upkeep. Budget $3,000 to $8,000 annually for routine maintenance alone, plus unexpected expenses that hit hard in years when seawalls fail or winter storms damage roofs. Many investors shock themselves when they realize these costs consume 40% to 60% of gross rental revenue, leaving thin margins that disappear with one bad season.

Property Taxes and Insurance Compound Your Carrying Costs

Property taxes on waterfront land run substantially higher than comparable inland parcels in most counties, sometimes double the rate. Flood insurance premiums add another $1,500 to $3,000 yearly depending on FEMA zone classification. Calculate total annual costs including property taxes, insurance, maintenance reserves, HOA fees if applicable, utilities you cover for renters, and property manager fees if you hire professional management (Up North Property Management, for example, handles full-service vacation rental management in Northern Minnesota, managing marketing, bookings, cleaning, and maintenance for homeowners).

Compare Lakefront Returns Against Other Investments

Single-family rentals in non-waterfront areas typically generate 8% to 12% annual returns on investment after all expenses, while lakefront properties targeting vacation renters often deliver 6% to 10% returns due to higher carrying costs. The premium pricing lakefront properties command gets partially offset by elevated operational expenses that most investors underestimate during the due diligence phase. If you cannot achieve at least 8% annual returns after accounting for realistic occupancy, maintenance reserves, and all carrying costs, the property fails your investment criteria regardless of how beautiful the view appears.

Final Thoughts

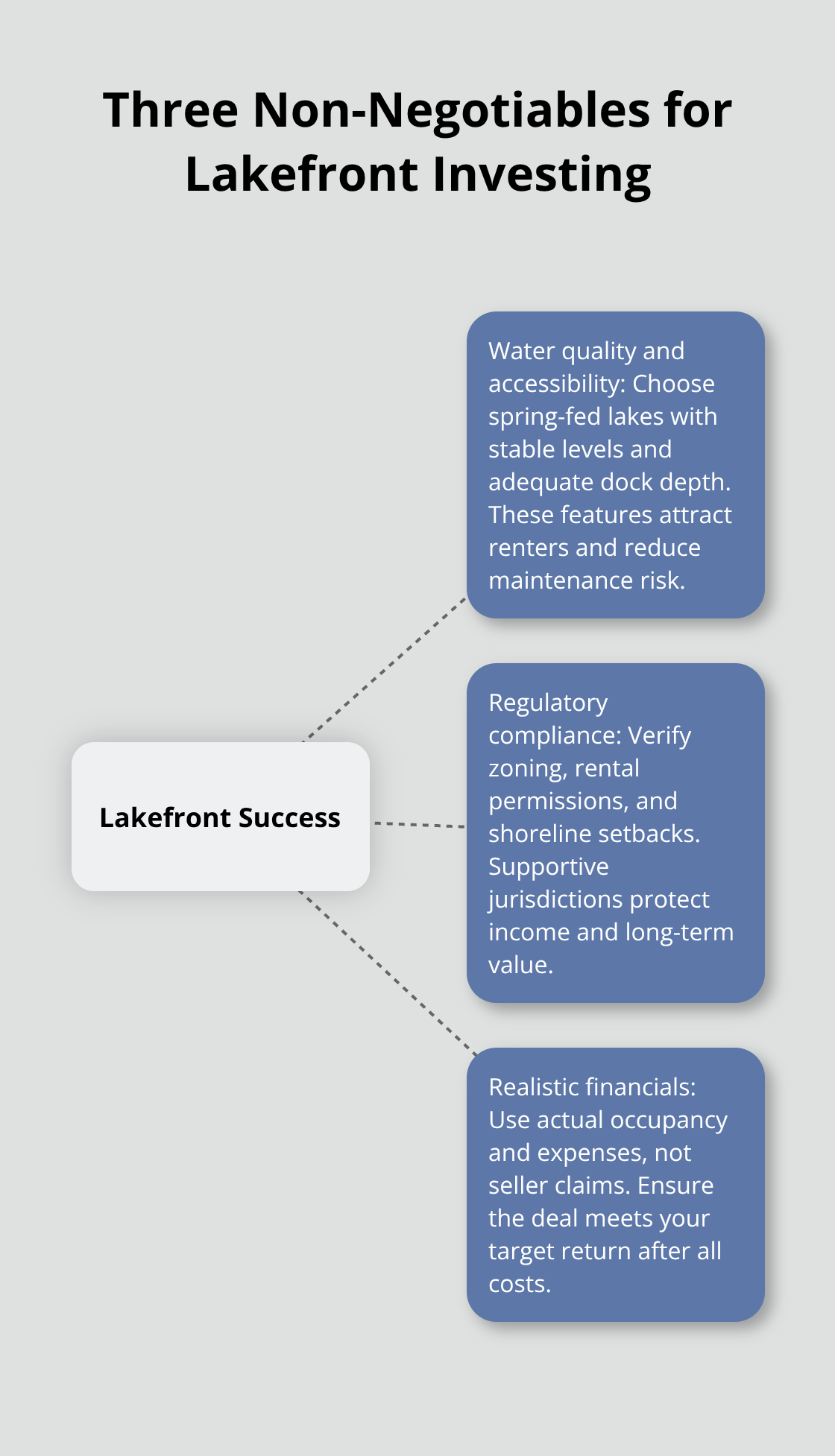

Successful lakefront property investment hinges on three non-negotiable factors: water quality and accessibility that attract renters, regulatory compliance that protects your rental income, and realistic financial projections that account for the true cost of ownership. Properties on spring-fed lakes with stable water levels, adequate dock depth, and locations near growing tourism markets outperform those in declining areas or restrictive jurisdictions.

The most beautiful lakefront property fails as an investment if you miscalculate occupancy rates, underestimate maintenance costs, or ignore zoning restrictions that prohibit short-term rentals.

The mistakes that destroy lakefront investments are predictable and avoidable. Investors routinely overestimate occupancy by 20% to 40%, ignore shoreline deterioration that costs $15,000 to $100,000 to repair, and skip regulatory due diligence only to discover their county prohibits vacation rentals. Property taxes on waterfront land run double the rate of inland parcels, and flood insurance premiums add thousands annually in high-risk zones-these carrying costs compress profit margins to unsustainable levels when combined with realistic occupancy rates and maintenance reserves.

Before committing capital to any lakefront property, pull actual booking data from comparable rentals, hire a professional engineer to inspect shoreline stability, and contact your county planning department to confirm rental permissions. If the property cannot generate at least 8% annual returns after all expenses, it fails your investment criteria regardless of view quality. We at Up North Property Management handle the operational complexity that derails many investors through full-service vacation rental management for Northern Minnesota properties, managing marketing, bookings, cleaning, and maintenance so you can focus on building wealth through lakefront property investment.