Vacation rental property owners leave thousands of dollars on the table every year by missing deductions they’re legally entitled to claim. At Up North Property Management, we’ve seen firsthand how proper tax planning transforms a property’s bottom line.

The difference between a mediocre tax return and an optimized one comes down to knowing what you can deduct and documenting it correctly. This guide walks you through the deductions available to you and the record-keeping systems that make claiming them straightforward.

What the IRS Actually Considers a Vacation Rental

The IRS doesn’t care what you call your property. It cares about how you use it and how much you rent it out. This distinction matters enormously because it determines which deductions you can claim and how much of your expenses are deductible.

A vacation rental property must provide sleeping space, a bathroom, and cooking facilities to qualify for residential rental treatment under IRS rules. That eliminates raw land, storage units, and parking spaces from consideration. The property itself can be a house, apartment, condominium, mobile home, motor home, or houseboat-the structure type is irrelevant. What matters is whether the IRS classifies it as a residence or a non-residence property based on your personal-use activity.

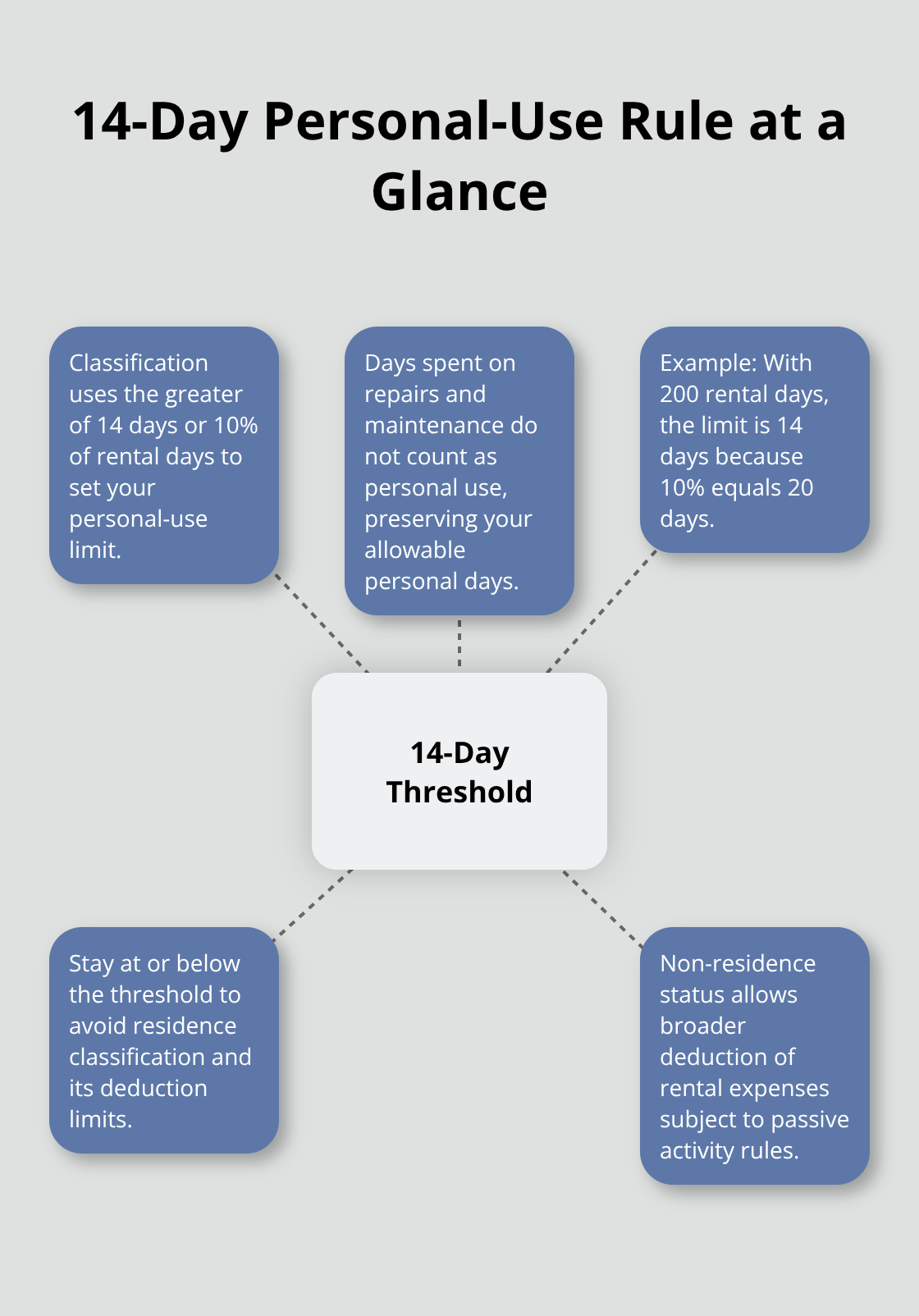

The 14-day personal-use threshold changes everything

The IRS uses a specific formula to determine if your property qualifies as a residence: the greater of 14 days or 10 percent of the total days you rent it at fair rental value. If your personal use stays at or below this threshold, the property is classified as a non-residence, and you can deduct rental expenses without the restrictive limitations that apply to residences.

Personal-use days include any day you or a family member occupy the property, or anyone with an ownership interest unless they pay fair rental value. Days you spend on repairs or maintenance do not count as personal use-a significant advantage if you actively improve the property. If you rent a vacation home for 200 days per year, your personal-use threshold is 14 days (since 10 percent of 200 equals 20 days, making 14 days the applicable limit). Stay under 14 days of personal use annually, and you avoid the residence classification entirely.

How rental income classification shapes your deductions

The IRS requires you to report all rental income on Schedule E, including advance rent, security deposits used as advance rent, and payments for canceling a lease. If a tenant pays any of your expenses directly, those amounts count as rental income. You must track rental days precisely because your deduction strategy depends on this classification.

Properties rented fewer than 15 days per year receive entirely different treatment-you don’t report rental income and cannot deduct rental expenses, though you can still claim standard homeowner deductions like mortgage interest and property taxes on Schedule A. Properties rented 15 or more days fall under the vacation-home rules, which require you to prorate expenses between personal and rental use. Non-residence properties, which have minimal or no personal use, allow you to deduct rental losses against other income subject to passive-activity loss limitations (potentially offsetting significant portions of your tax liability).

Understanding residence versus non-residence status

Your property’s classification determines your entire tax strategy. A residence property limits your deductible expenses to the amount of rental income you receive, which means excess deductions carry forward to future years. A non-residence property removes this income limitation, allowing losses to offset other income on your return.

The residence classification applies when personal use exceeds the 14-day threshold. This triggers the proration requirement-you must allocate mortgage interest, property taxes, and other expenses based on the ratio of rental days to total days used. The order of deduction matters: you deduct rental portions of mortgage interest and property taxes first, then casualty losses, then direct rental expenses, and finally depreciation. Understanding which category your property falls into before tax season arrives prevents costly mistakes and missed deductions.

What You Can Actually Deduct

The gap between what vacation rental owners think they can deduct and what the IRS actually allows is where most owners lose money. Once you understand the four major deduction categories, you’ll stop leaving legitimate tax savings unclaimed.

Mortgage Interest, Property Taxes, and Direct Expenses

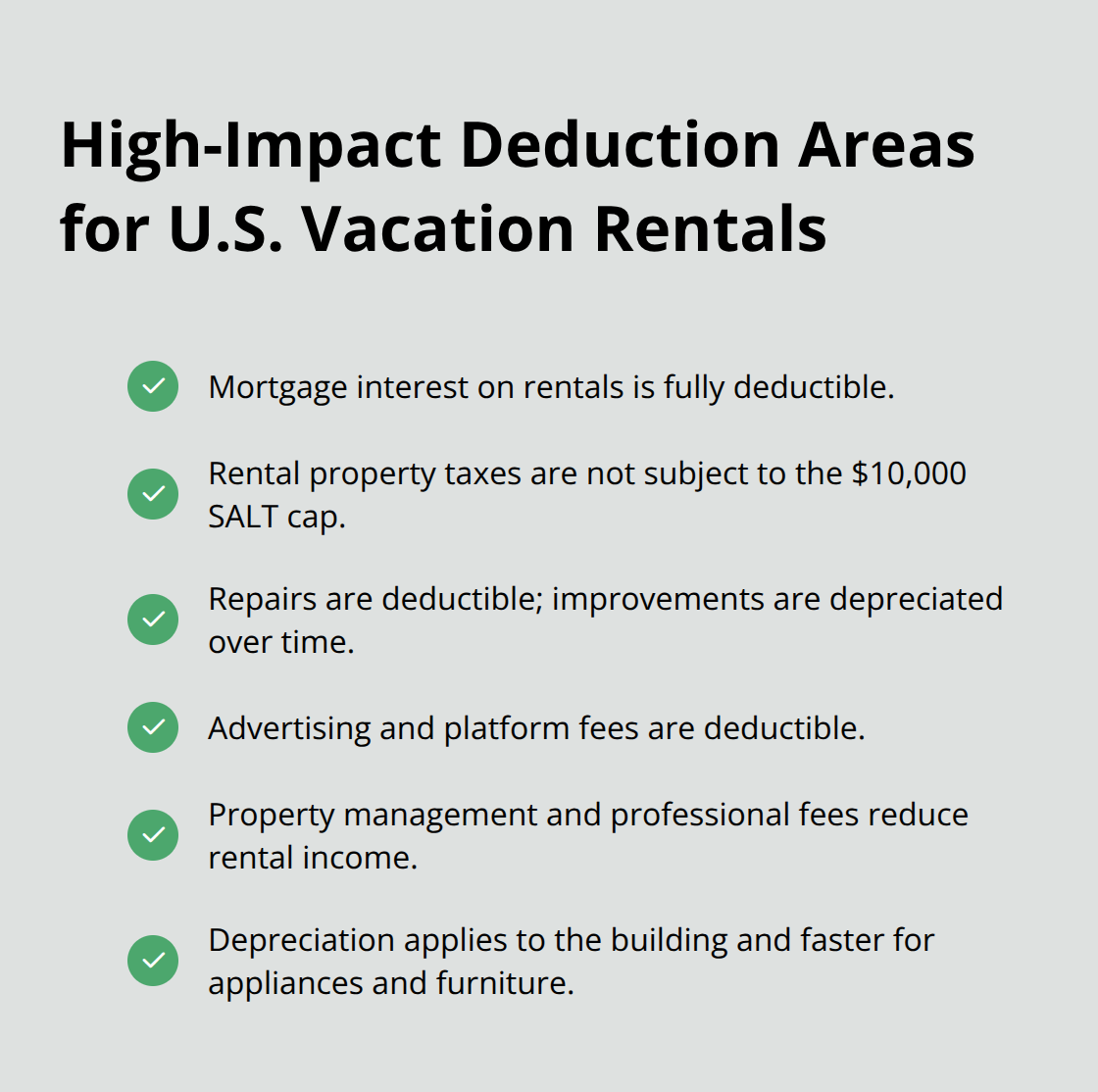

Mortgage interest on rental properties receives full deduction treatment with no limits, unlike the $750,000 cap that applies to primary residences. Property taxes on your rental also get deducted without the $10,000 state and local tax cap that restricts personal property tax deductions. If you own a property generating $50,000 in annual rental income with $15,000 in mortgage interest and $4,000 in property taxes, those $19,000 in deductions directly reduce your taxable rental income.

Utilities, insurance premiums, maintenance costs, and repairs all qualify as ordinary and necessary rental expenses that lower your taxable income dollar-for-dollar. The distinction between repairs and improvements matters tremendously-replacing a worn roof is a repair you deduct immediately, while installing a completely new roof system is an improvement that gets depreciated over 27.5 years.

Platform Fees and Management Costs

Advertising costs on platforms like Airbnb and Vrbo are fully deductible, as are marketplace fees those platforms charge. Management fees, whether you pay a property manager or handle operations yourself, office supplies, legal fees, and cleaning supplies all reduce your rental income on Schedule E.

Depreciation and Asset Deductions

Depreciation is where owners frequently miss substantial deductions. The building structure itself depreciates over 27.5 years, but appliances, furniture, and fixtures depreciate faster under bonus depreciation rules, allowing you to deduct portions of these asset costs in the first year under current tax law.

Documentation and Special Situations

Treating your vacation rental as a business from day one, not as a hobby or side income, determines how effectively you claim deductions. Owners who maintain meticulous records of every expense-from towels and guest amenities to airfare for repair trips-can substantiate deductions the IRS will actually accept if questioned. Travel expenses for rental property repairs must be documented under IRS Publication 463, meaning you need dates, destinations, and the business purpose clearly recorded.

If you provide services beyond basic rental (such as coffee, breakfast, or premium concierge amenities), the IRS may classify you as self-employed, triggering self-employment taxes on top of income tax, so track what you offer carefully. Occupancy and lodging taxes collected from guests are not deductible on your federal income tax return-they’re separate obligations to state and local authorities. The most overlooked deduction involves allocating home office expenses if you manage the rental from home; equipment, supplies, and a proportionate share of your home costs become deductible business expenses.

Tracking which days your property was rented versus personally used determines how much of shared expenses like mortgage interest and property taxes you can deduct, making accurate day-counting essential for your entire deduction strategy. This precision in record-keeping sets the foundation for the next critical step: organizing your documentation in a way that withstands IRS scrutiny and maximizes every dollar you’re entitled to claim.

How to Track Expenses Without Losing Your Mind

The difference between vacation rental owners who claim $8,000 in deductions and those who claim $15,000 comes down to one thing: documentation systems. You cannot deduct what you cannot prove, and the IRS will reject vague expense categories or unsupported claims. Most owners fail not because they lack deductible expenses, but because they never organized them in the first place.

Treat expense tracking as a non-negotiable business function, not an afterthought. Create a dedicated folder, either physical or digital, where every receipt lands immediately after purchase. Photograph receipts the moment you receive them if you pay cash, because paper fades and gets lost.

Document Everything the IRS Expects

For expenses over $75, the IRS expects you to maintain contemporaneous written documentation showing the date, amount, location, and business purpose. A credit card statement alone won’t suffice for a $200 repair bill. Write on the receipt itself what was repaired and why it matters to your rental business.

When you purchase supplies like towels, cleaning products, or guest amenities, document the quantity and intended use for the property. If you travel to your rental property for repairs, record your departure date, return date, destination, mileage or airfare cost, and the specific repairs or maintenance you performed. IRS Publication 463 requires this level of detail for travel expenses, and owners who skip this step regularly lose deductions worth hundreds of dollars annually.

Track Personal-Use Days Versus Rental Days

Your second critical system tracks personal-use days versus rental days, which determines your entire deduction strategy. Create a simple calendar or spreadsheet marking each day as either rented, personally used, or vacant. Days when you or family members stay at the property count as personal use. Days when anyone with an ownership interest occupies the property without paying fair rental value also count as personal use.

Days spent on repairs and maintenance do not count as personal use, so if you spend three days replacing flooring, those days remain available for rental or personal use classification. At year-end, count your totals and calculate whether you hit the 14-day personal-use threshold. If you rented the property 200 days and used it personally for 12 days, you stayed under the threshold and achieved non-residence status, meaning your deductions face no income limitations.

This single calculation determines whether your rental losses offset other income or carry forward indefinitely. Most owners guess at these numbers instead of tracking them, which creates audit risk and leaves deductions unclaimed. Your calendar becomes your defense if the IRS questions your deduction claims.

Choose Your Tracking Tools Wisely

Accounting software like QuickBooks Self-Employed or Wave automatically timestamps expenses and generates category reports, but a basic spreadsheet works equally well if you update it weekly rather than scrambling to reconstruct the year in December. The tool matters far less than the consistency with which you use it.

Organize Receipts Into Tax-Ready Categories

Divide your expenses into the five categories the IRS recognizes: mortgage interest and property taxes, utilities and insurance, repairs and maintenance, advertising and management fees, and depreciation. When you receive a utility bill, immediately note whether it covers the rental property exclusively or includes your personal residence. If the bill covers both, calculate the rental percentage based on square footage or usage days and record only the rental portion.

For insurance, your homeowner or landlord policy documents the premium amount and coverage period. Maintenance receipts require notation of what was fixed and why. A $300 plumbing bill becomes deductible when you write on the receipt that you replaced a broken toilet in the master bathroom. A $1,200 roof repair claim gains credibility when you attach photos showing the damage and the completed work.

Platform fees from Airbnb or Vrbo appear in your account statements and transfer directly into your advertising and fees category. At tax time, sum each category and enter the totals on Schedule E. Owners who organize this way spend 30 minutes at tax time compiling their return. Owners who don’t spend 6 hours scrambling to find receipts and reconstructing expenses from memory, and they inevitably miss legitimate deductions worth thousands of dollars annually.

Final Thoughts

Vacation rental property tax deductions require three commitments: understanding which expenses qualify, documenting everything meticulously, and recognizing when professional guidance becomes essential. You now know the IRS classification rules that determine your deduction strategy, the specific expenses that reduce your taxable income, and the tracking systems that make claiming deductions defensible. The owners who capture the most tax savings aren’t necessarily those with the highest rental income-they’re the ones who treat their vacation rental as a legitimate business from day one.

Your documentation systems directly translate into dollars saved. A property manager who tracks personal-use days precisely, organizes receipts by category, and records business purposes on every expense claim will deduct thousands more than an owner who guesses at numbers and loses receipts. The difference between claiming $8,000 and $15,000 in annual deductions often comes down to whether you documented travel expenses for repairs, captured platform fees, and allocated home office costs correctly.

Vacation rental property tax deductions exist within a complex framework of IRS rules that change based on your specific situation. A tax professional who specializes in rental property can identify deductions you’d miss on your own and structure your business to minimize tax liability legally. If operational management feels overwhelming, Up North Property Management handles marketing, bookings, cleaning, and maintenance for vacation rentals in Northern Minnesota, freeing you to focus on the tax and financial strategy side of your business.