Minnesota’s cabin market is heating up, and the timing might be perfect for your cabin investment strategy. Property values in the north are climbing, remote workers are relocating, and vacation rental demand keeps growing.

At Up North Property Management, we’ve watched this market shift dramatically over the past few years. The question isn’t whether cabins are worth buying-it’s whether you’re ready to act before inventory tightens further.

What’s Happening to Minnesota Cabin Prices Right Now

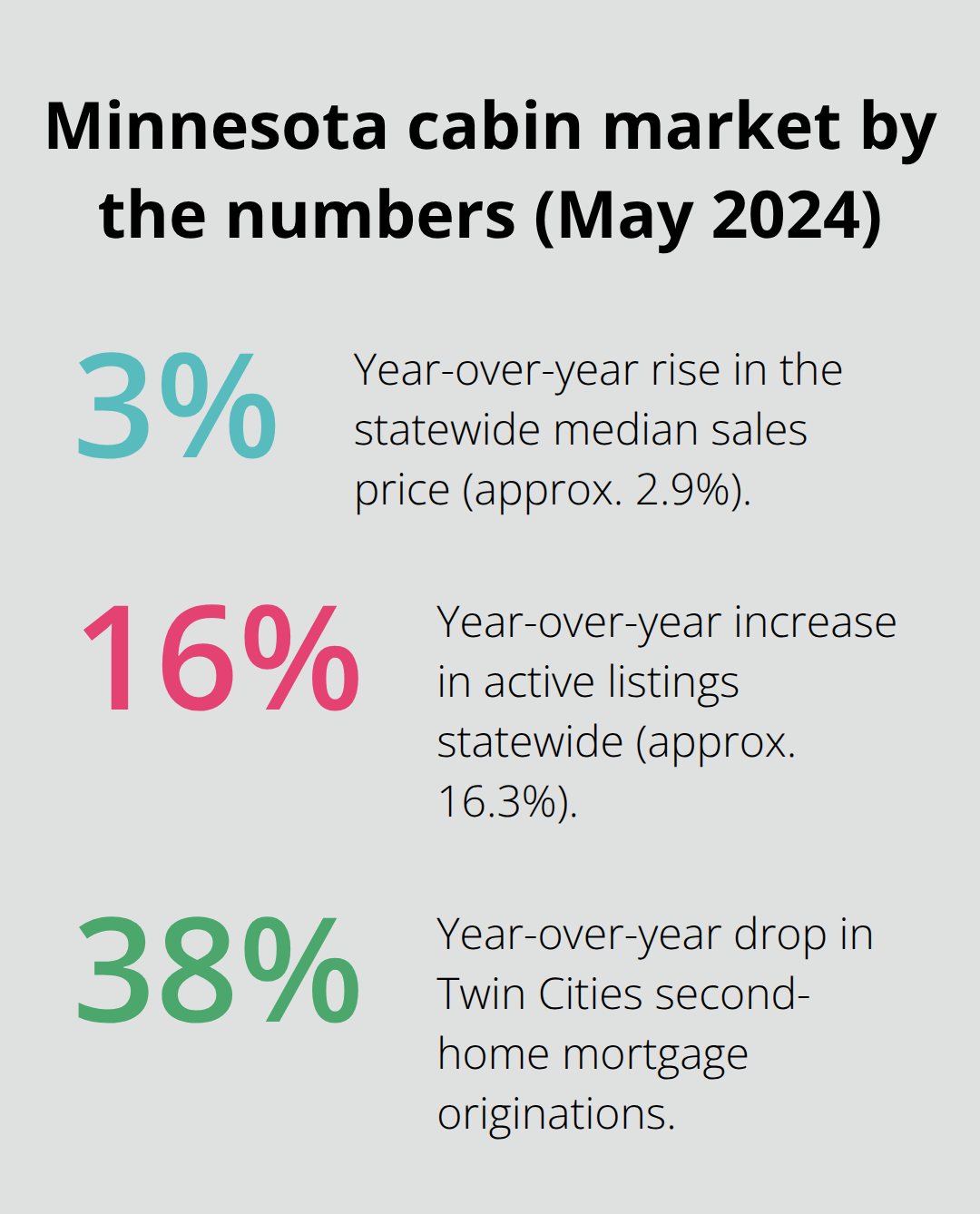

Minnesota’s cabin market is tightening, and prices reflect it. According to Minnesota Realtors data from May 2024, the statewide median sales price climbed to $350,000, up 2.9% year-over-year. In northern markets like Hibbing and Grand Rapids, price gains were even steeper. Active listings expanded to 13,910 statewide that month-a 16.3% jump-but this growth masks a critical reality: inventory remains undersupplied relative to demand. The market sits at roughly 2.5 months of supply statewide, well below the 4–6 months needed for balance. Properties in the Twin Cities metro sell even faster, with buyers accepting 100.1% of list price in 40 days.

For cabin investors, this means two things. First, properties in hot zones like Bemidji, Detroit Lakes, and Fergus Falls move quickly when priced right. Second, the window to buy before prices climb further is narrowing, particularly in markets where new listings remain scarce.

Where Demand Is Actually Coming From

Remote work fundamentally shifted who buys Minnesota cabins. Pandemic-era relocations created sustained demand that hasn’t reversed, even as mortgage rates climbed and second-home lending tightened nationwide. Redfin’s analysis shows second-home mortgage originations fell twice as fast as primary-home demand, with Twin Cities metro second-home originations down 38% year-over-year. Yet sales continue, which means buyers who pay cash or carry historically low rates from years past remain active. Vacation rental demand stays strong-lakefront properties in particular attract consistent bookings during peak seasons. However, this demand is seasonal and concentrated. August saw 395 closings versus lower activity in winter months. The practical implication: your cabin must perform well during seasonal peaks if rental income is your primary goal. Buyers with higher mortgage rates today need stronger cash-flow assumptions to justify the purchase price.

Why Regional Location Matters More Than Ever

Not all Minnesota cabin markets are equal right now. St. Cloud, Rochester, the Twin Cities, and Mankato rank as the most undersupplied areas, meaning competition is fierce and prices reflect it. Grand Rapids was the only region in Minnesota posting more new listings year-over-year in May 2024. Bemidji, Detroit Lakes, and Fergus Falls showed more balanced supply-demand conditions-attractive for buyers who want less competition and potentially better negotiating leverage. Rural Minnesota’s faster sale activity in some areas signals opportunities where inventory is actually improving. If you’re serious about cabin investment, location strategy matters more than ever. A property in an undersupplied metro-adjacent market will appreciate faster but demands a higher entry price and faces stiffer competition. A cabin in a more balanced rural market gives you time to negotiate and potentially stronger rental fundamentals if you’re buying for income.

The Rental Income Question

Vacation rental income can offset your mortgage and property costs, but only if you position your cabin correctly. Properties that attract bookings year-round or during peak summer months generate the strongest returns. Seasonal fluctuations mean winter months typically produce lower occupancy rates, so your financial model must account for this reality. Properties in undersupplied markets command higher nightly rates, but they also face stiffer competition from other rentals. A cabin in a more balanced market may offer steadier bookings at slightly lower rates. Professional management companies handle marketing, bookings, and maintenance-services that cost money but free you from day-to-day operations. The decision between self-management and professional services depends on your time availability and how much you value hands-off ownership.

Timing Your Entry Into the Market

The current market conditions create both urgency and opportunity. Inventory is expanding (13,910 active listings statewide in May 2024), which means more options exist than a year ago. However, prices continue climbing, and properties in hot markets sell within 40 days. If you wait for rates to drop or inventory to surge further, you risk paying higher prices when you finally act. Markets like Bemidji, Detroit Lakes, and Fergus Falls offer more balanced conditions than the Twin Cities, which means you have more time to evaluate properties and negotiate. The next section examines the financial benefits that make cabin ownership attractive beyond just appreciation and rental income.

How Cabin Ownership Builds Real Wealth

Cabin ownership in Minnesota generates income through multiple streams, and the numbers justify the investment if you structure it correctly.

Vacation Rental Income: The Direct Path

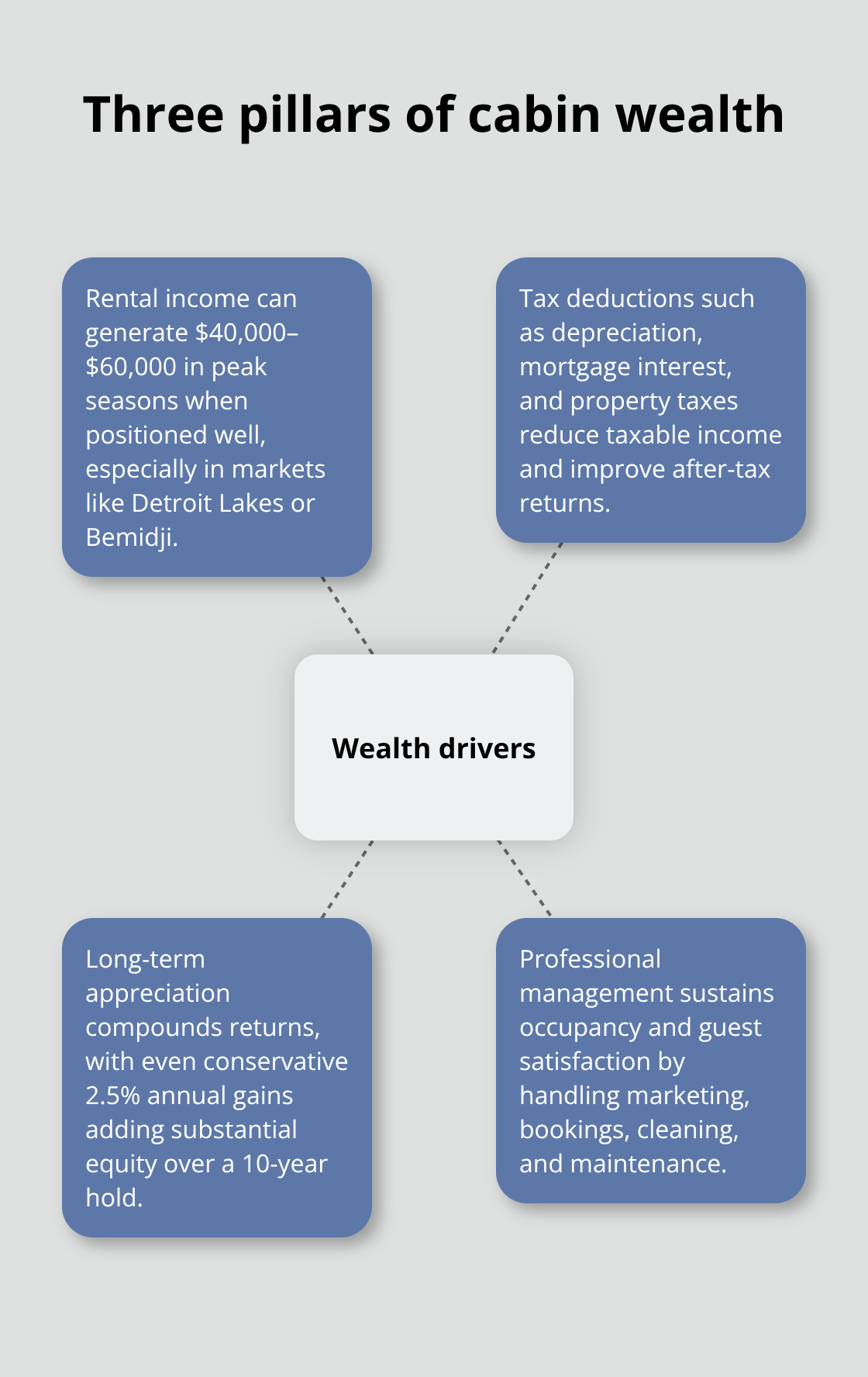

Vacation rental income remains the most direct wealth builder. A cabin in a market like Detroit Lakes or Bemidji can generate $40,000 to $60,000 annually during peak seasons, depending on size, amenities, and positioning. However, this income requires disciplined management. Properties that rent year-round perform better than seasonal-only cabins, but Minnesota’s climate means winter bookings demand premium insulation, heated spaces, and snow removal budgets.

The rental income question isn’t theoretical-it’s about whether your specific property will sustain occupancy rates high enough to cover the mortgage, property taxes, insurance, utilities, and maintenance. A cabin generating $50,000 in gross rental revenue loses roughly 30 to 40 percent to operating expenses and management fees if you use professional services. That leaves $30,000 to $35,000 in net income. If your purchase price was $400,000, that translates to a 7.5 to 8.7 percent annual return before appreciation. Compare that to stock market returns or bond yields, and the math becomes compelling, especially when paired with long-term property appreciation.

Tax Deductions That Shield Your Income

Tax advantages amplify this return significantly. The IRS allows depreciation deductions on rental cabins over 27.5 years, which means you deduct a portion of the property’s value each year as an expense, reducing your taxable rental income even though you didn’t actually spend cash. For a $400,000 cabin with $100,000 in land value, the remaining $300,000 depreciates over 27.5 years, generating roughly $10,900 in annual depreciation deductions. This shields rental income from taxation and creates what accountants call phantom income shelter.

Mortgage interest is also fully deductible on investment properties, further reducing your tax burden. State property taxes in Minnesota vary by county but typically range from 0.8 to 1.1 percent of property value annually, and these are deductible against rental income. A cabin purchased for $400,000 in a county with a 1 percent effective tax rate generates $4,000 in annual property tax deductions. Combined with depreciation and mortgage interest, you shield a substantial portion of your rental income from federal and state taxes. Work with a tax professional familiar with vacation rental properties to maximize these benefits-the savings often exceed $5,000 to $10,000 annually depending on your income bracket and property specifics.

Long-Term Appreciation: The Wealth Multiplier

Long-term appreciation completes the wealth-building equation. Minnesota’s cabin market has experienced appreciation, with northern markets like Hibbing and Grand Rapids posting gains. Over a 10-year hold period, even conservative 2.5 percent annual appreciation on a $400,000 cabin adds roughly $270,000 in equity before accounting for mortgage paydown. If you finance 80 percent of the purchase price, your initial $80,000 down payment gains $270,000 in appreciation value alone, tripling your initial capital.

This combination-rental income, tax deductions, and property appreciation-creates a wealth-building engine that outpaces passive investments for disciplined investors. The key is buying in the right location, pricing it competitively for rentals, and managing it professionally to sustain occupancy and guest satisfaction.

Professional management companies handle marketing, bookings, cleaning, and maintenance, ensuring properties stay in top condition while you collect income without the operational headaches. The next section examines the real challenges that separate successful cabin investors from those who struggle with their investment.

The Real Costs of Cabin Ownership

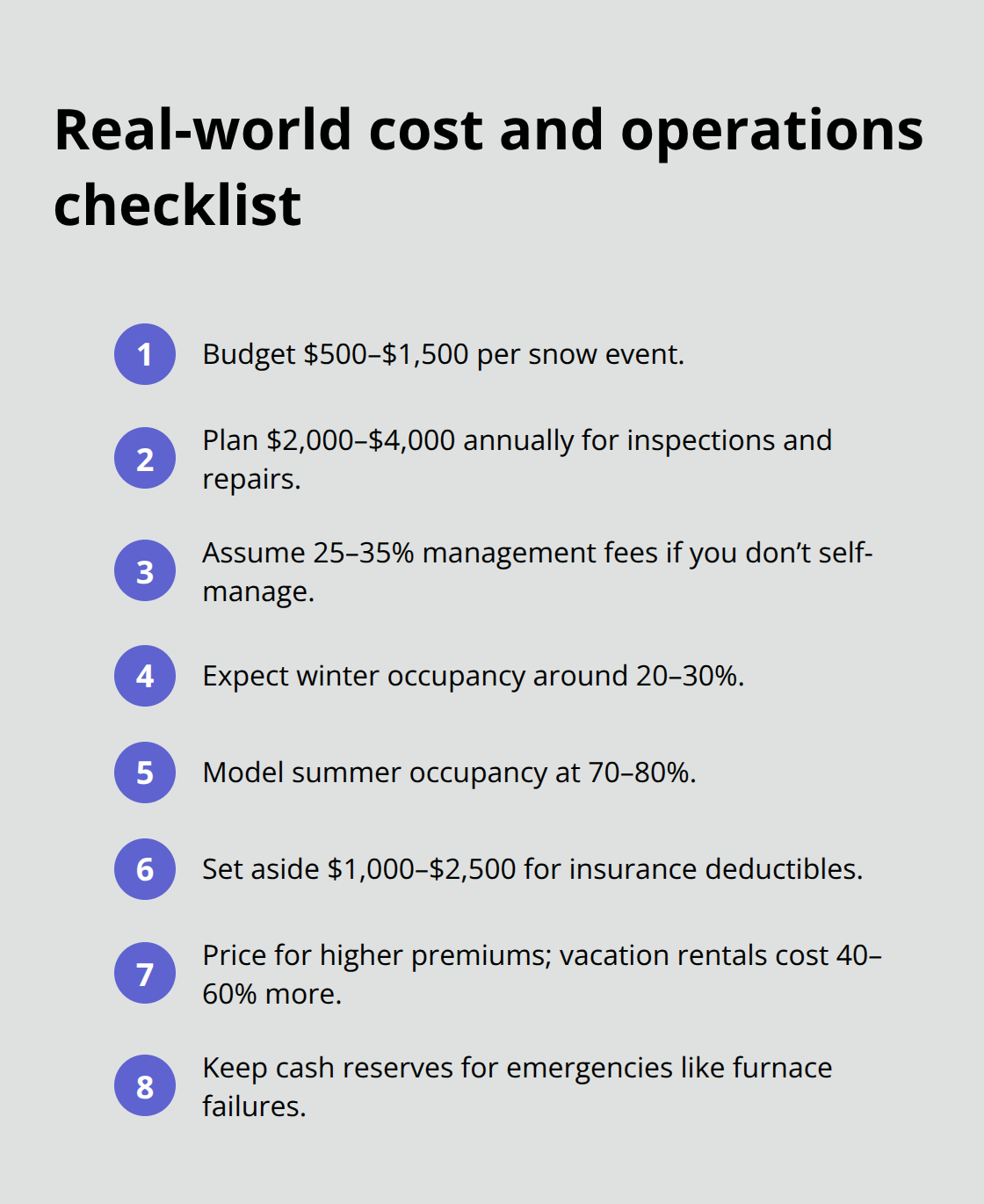

Cabin ownership in Minnesota looks attractive on paper until you face the operational reality. Seasonal demand creates income volatility that catches many investors off guard. August produces strong bookings, but January and February see occupancy rates drop significantly below peak season. Your cabin might earn $8,000 monthly in July but only $2,000 in February. If you financed the property with a $3,000 monthly mortgage payment, winter months force you to cover the gap from savings or other income. This seasonal pattern is unavoidable in Minnesota’s climate, and no amount of marketing fixes it. Properties that succeed financially operate on conservative cash-flow models that assume winter occupancy rates of 20 to 30 percent, not the 70 to 80 percent rates achievable in summer. Your financial projections must reflect this reality, not a best-case scenario.

Property Management Demands Real Time and Money

Property management and maintenance consume far more time and money than most owners anticipate. A cabin sitting empty between guests still requires snow removal in winter, which costs $500 to $1,500 per event depending on property size and location. Roof inspections, septic system maintenance, dock repairs, and winterization add another $2,000 to $4,000 annually. If you self-manage, you handle guest communications, coordinate cleaning, schedule maintenance, and answer emergency calls at 2 a.m. when the furnace fails. If you hire professional management, you pay 25 to 35 percent of gross rental revenue. On a cabin producing $50,000 annually, that amounts to $12,500 to $17,500 in management fees.

Insurance Costs Have Risen Sharply

Vacation rental policies cost 40 to 60 percent more than standard homeowner coverage because of liability exposure. Weather-related risks in Minnesota are real and expensive. Ice dams cause interior water damage costing $5,000 to $15,000 to repair. Frozen pipes crack during harsh winters, and spring thaws sometimes flood basements. Deductibles on weather-related claims often run $1,000 to $2,500, meaning smaller incidents come out of pocket. Liability claims from guest injuries are catastrophic without proper coverage. Minnesota courts award substantial damages in premises liability cases, and a single serious injury claim can exceed $500,000. Umbrella policies covering vacation rentals are non-negotiable for protecting your investment. These costs aren’t negotiable or avoidable-they’re built into cabin ownership in this climate. Investors who succeed account for every expense in their financial models and maintain adequate insurance coverage.

Final Thoughts

The Minnesota cabin market tightens as inventory remains constrained relative to demand, with active listings at 13,910 statewide but months of supply hovering around 2.5 months. Properties in undersupplied markets like the Twin Cities and St. Cloud sell within 40 days, and prices continue climbing. If you delay your cabin investment decision, you risk paying significantly more when you finally commit.

Tourism to Northern Minnesota’s lakes region continues growing, driven by remote workers seeking lifestyle changes and vacationers escaping urban areas. Markets like Bemidji, Detroit Lakes, and Fergus Falls show more balanced conditions than metro areas, giving you time to evaluate properties without the pressure of bidding wars. These regions attract consistent vacation traffic while offering more reasonable entry prices than Twin Cities-adjacent markets.

The operational complexity of cabin ownership demands professional support, and we at Up North Property Management handle the full operational burden-managing marketing, bookings, cleaning, and maintenance so your property attracts consistent bookings while you focus on other priorities. Rental income, tax deductions, and property appreciation combine to build wealth faster than passive investments when you structure your cabin investment correctly. The convergence of limited inventory, growing tourism demand, and access to professional management creates a rare opportunity to act now while balanced markets still exist.