Owning a vacation rental in Minnesota comes with real tax obligations that many owners overlook. The IRS requires you to report all rental income, and Minnesota adds its own state taxes on top of federal requirements.

At Up North Property Management, we’ve seen owners face penalties and missed deductions simply because they didn’t understand vacation rental taxes in Minnesota. This guide walks you through exactly what you owe and how to stay compliant.

Federal Income Tax Requirements for Vacation Rentals

What You Must Report to the IRS

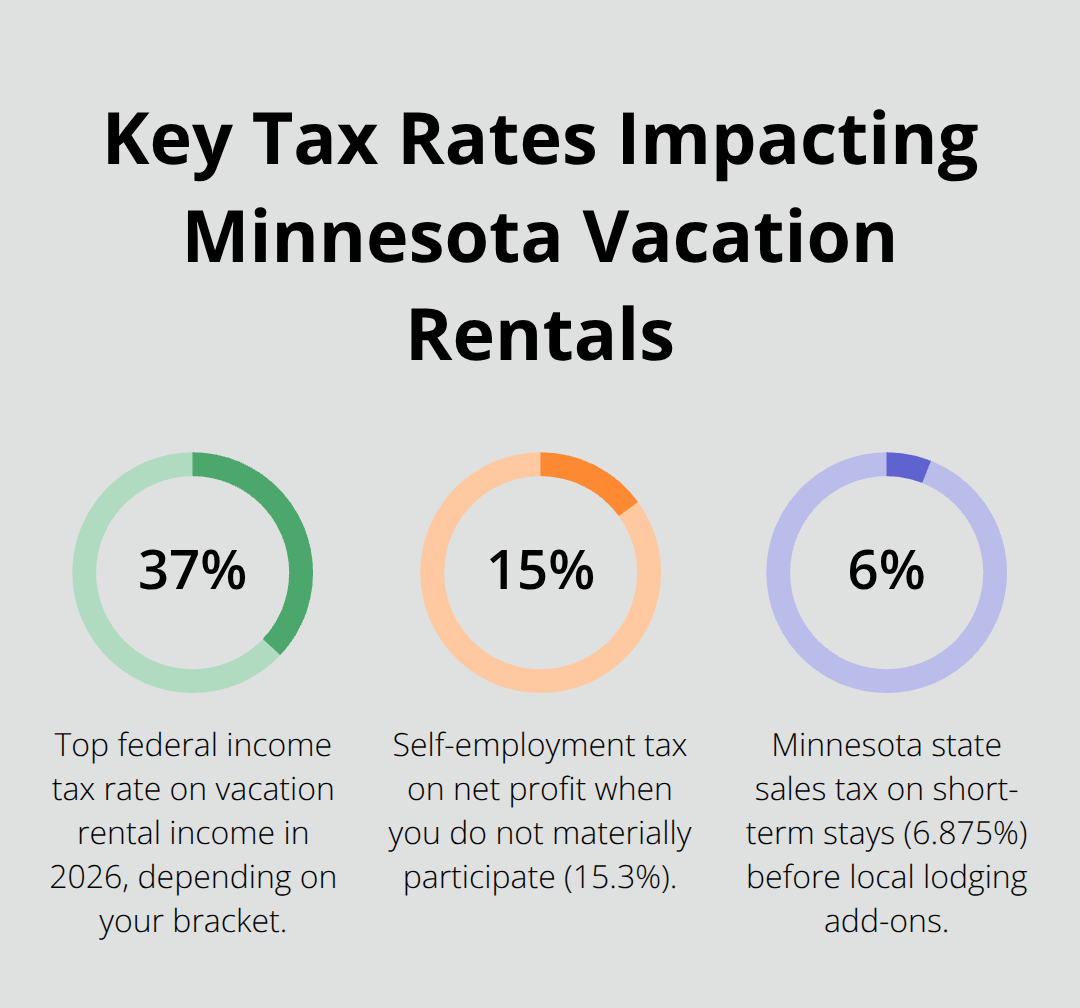

The IRS treats vacation rental income as ordinary business income, not passive investment income. You report all rental receipts on Schedule E of Form 1040, and the federal income tax rate on this income reaches up to 37% in 2026 depending on your tax bracket. This means a $50,000 rental profit costs you up to $18,500 in federal taxes alone. The IRS does not care whether you use Airbnb, VRBO, or collect payments directly-you must report all income. Many owners attempt to hide cash bookings or underreport income, but the IRS has increasingly targeted vacation rental operators with audits. If you operate through a marketplace, that platform sends Form 1099-K to the IRS when your transaction volume exceeds certain thresholds, creating a permanent record.

One critical mistake owners make is reporting only the net amount after expenses. You must report gross rental income first, then deduct legitimate expenses separately. This distinction matters because the IRS cross-references 1099-K amounts with your reported income.

Deductions That Reduce Your Tax Bill

Vacation rental owners can deduct far more than most realize, but only if expenses relate directly to producing rental income. Mortgage interest on the rental qualifies for a full deduction up to $750,000 of debt for married couples filing jointly. Property taxes, insurance, utilities, maintenance, repairs, and cleaning all qualify. Furniture and appliances depreciate over 5 to 7 years, while the building itself depreciates over 27.5 years-this depreciation can save thousands annually without touching your bank account. A $500,000 property might generate $40,000 to $60,000 in additional first-year deductions through cost segregation analysis, which accelerates depreciation on personal property and building components. Advertising costs, property management fees, HOA dues, and even your accountant’s fees are deductible. The key is separation: track rental expenses in their own account or spreadsheet, never mixing personal and business spending.

Self-Employment Tax and Entity Structure

Self-employment tax on rental income depends on whether you materially participate in the business. If you spend 500 or more hours annually managing the property, making decisions, or handling guest relations, the IRS classifies you as materially participating. Without material participation, you owe self-employment tax at 15.3% on net profit. With material participation, you might benefit from an S Corporation election through an LLC, which lets you pay yourself a reasonable W-2 salary and take remaining profits as distributions-saving roughly $6,100 annually on a $100,000 profit because distributions avoid self-employment tax. Your entity structure directly impacts how much you owe in federal taxes, so the choice between sole proprietor, LLC, and S Corporation matters significantly. Minnesota state taxes add another layer to your federal obligations, and understanding both requirements together helps you plan your overall tax strategy.

Minnesota Taxes on Vacation Rental Income

Minnesota adds state income tax and lodging taxes on top of your federal obligations, creating a multi-layer tax structure that catches many owners off guard. Minnesota state income tax on vacation rental profits ranges from 5.35% to 9.85% in 2026, depending on your overall income level, according to the Minnesota Department of Revenue. This means that $50,000 rental profit faces roughly $2,675 to $4,925 in Minnesota state taxes alone, stacked on top of federal taxes. The state taxes your net rental income after deductions, so maximizing deductible expenses directly reduces your Minnesota tax bill. Unlike federal taxes where the rate depends on your bracket, Minnesota’s progressive rate structure means higher earners pay the top 9.85% rate on rental income. If you sell the property later, Minnesota imposes long-term capital gains tax up to 9.85% on appreciation, plus federal capital gains rates.

Understanding Minnesota’s Lodging Tax Structure

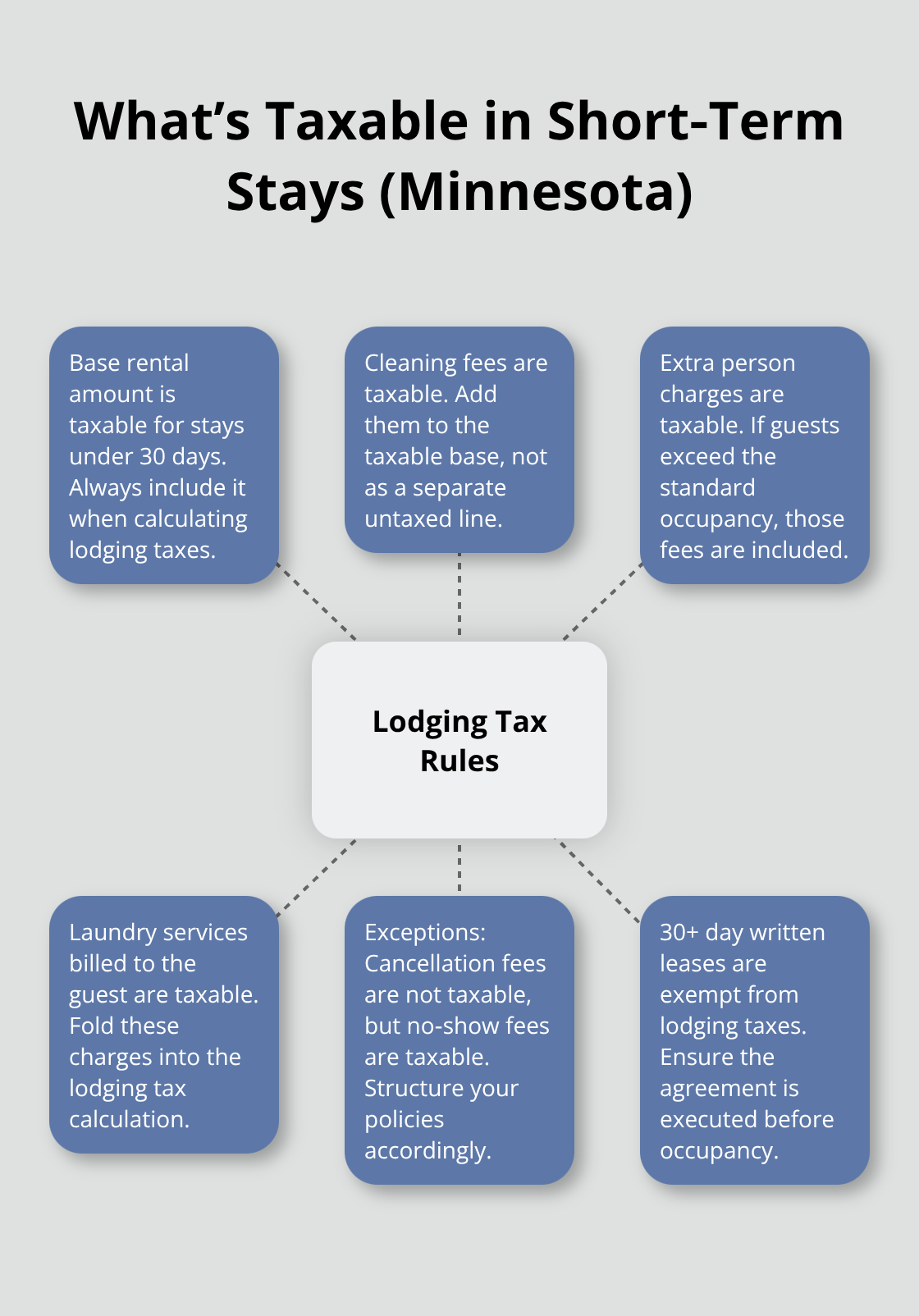

Minnesota requires you to collect sales tax on short-term rentals under 30 days, but the rate varies dramatically by location. State sales tax sits at 6.875%, but most cities add local lodging taxes ranging from 3% to 5%, creating combined rates between 9.875% and 11.875% depending on where your property sits. Minneapolis imposes special local lodging taxes on top of the standard rate, making it one of the higher-tax jurisdictions in the state. The Minnesota Department of Revenue’s lodging tax lookup tool shows your exact combined rate and registration requirements when you enter your property address. The tool reveals whether you must file monthly, quarterly, or annually, plus the minimum rental days needed to trigger tax collection for your address.

Navigating Platform Tax Collection Gaps

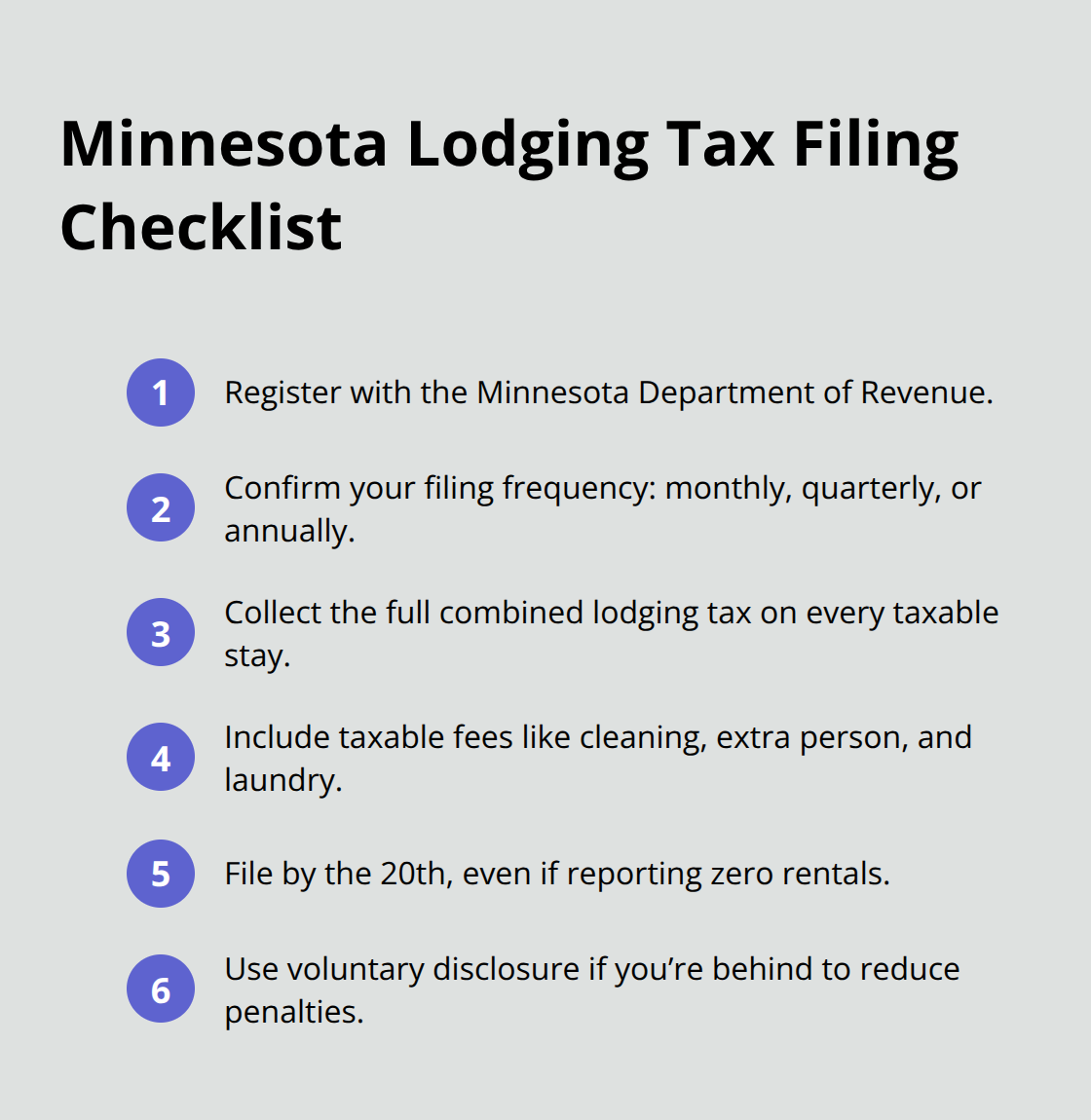

Many owners operating through Airbnb or VRBO assume the platform handles all taxes, but platforms typically collect state sales tax while leaving local lodging taxes to the property owner. This creates a compliance gap where you remain responsible for unpaid local taxes even if the marketplace claims to handle everything. Registration with the Minnesota Department of Revenue happens online and costs nothing, but filing late brings penalties and interest that compound quickly. Even if you had zero rentals during a filing period, registered hosts must submit zero-dollar returns or face penalties.

Collecting and Remitting Lodging Taxes Correctly

Add all applicable taxes to your guest’s bill at the time of payment, not after the fact. If your property sits in a jurisdiction with a 10.5% combined lodging tax rate and a guest books a $1,000 stay, you collect $105 in lodging taxes upfront and remit that to Minnesota authorities on your filing deadline.

Lodging-related charges beyond the base rental amount are also taxable, including cleaning fees, pet fees, extra person charges, and laundry services. Cancellation fees are not taxable, but no-show fees are, so structure your cancellation policy carefully. Properties with enforceable written leases for 30 or more days avoid lodging taxes entirely, but the lease must be in place before occupancy begins and include proper termination clauses. Without that written agreement, even a five-week stay triggers full lodging tax liability.

Filing Deadlines and Enforcement

File lodging tax returns according to your assigned frequency, with monthly returns due the 20th of the following month and quarterly returns due the 20th of the following quarter. Late filing brings immediate penalties, and Minnesota Department of Revenue enforcement has tightened considerably in recent years.

If you haven’t collected lodging taxes in prior years, a voluntary disclosure agreement with the state may waive penalties and interest on back taxes, making it worth contacting the department immediately rather than waiting for an audit. Understanding your local tax obligations sets the foundation for proper record-keeping, which becomes your strongest defense against compliance issues and audit exposure.

Record-Keeping and Compliance Best Practices

Separate Your Rental Finances From Personal Spending

Separating rental finances from personal spending is non-negotiable if you want to survive a Minnesota Department of Revenue audit. Open a dedicated checking account for all vacation rental income and expenses, then use accounting software like QuickBooks or Wave to categorize transactions in real time rather than scrambling to organize receipts at tax time. The moment you deposit guest payments or pay for repairs, log them immediately with the property address and expense category. Many owners wait until March to gather records, only to discover missing receipts and vague transactions that trigger audit flags. Your bank statements and credit card statements become the backbone of your defense during an audit, so the Minnesota Department of Revenue expects you to produce them alongside your tax return. If you claim $8,000 in cleaning expenses but your bank shows only $6,200 in actual payments, the discrepancy invites questions.

Document Everything With Precision

Document everything: screenshots of your Airbnb or VRBO calendar showing rental dates, guest communications, maintenance invoices with the property address clearly stated, utility bills showing the rental period, and insurance policies specific to the vacation rental. The IRS requires you to distinguish between personal use days and rental days because the allocation of expenses depends on this split. If you stayed at the property 30 days and rented it 120 days in a year, you can only deduct 120/150 of your property taxes and mortgage interest. Maintain a calendar or spreadsheet tracking every single day the property was occupied, by whom, and whether it was a personal stay, rental, or maintenance period. This documentation becomes critical when the Minnesota Department of Revenue questions whether you materially participated in the business, which determines your self-employment tax liability. Keep records showing hours spent on guest communication, property decisions, maintenance coordination, and marketing activities. A simple spreadsheet with dates and hours spent on each activity protects you if auditors challenge whether you qualify for S Corporation treatment or passive income classification.

Work With a Tax Professional Who Understands Vacation Rentals

Hiring a tax professional who understands Minnesota vacation rental operations is worth far more than you’ll pay them. A competent accountant catches deductions you miss, structures your entity to minimize taxes legally, and handles the complexity of depreciation recapture when you eventually sell. They file your federal return, Minnesota state return, and coordinate with the Minnesota Department of Revenue on lodging tax compliance, ensuring nothing falls through the cracks. Many owners attempt to handle taxes alone and miss opportunities like cost segregation studies that could save thousands, or they fail to file required zero-dollar lodging tax returns in slow months, accumulating penalties. The cost of a tax professional typically ranges from $1,500 to $3,500 annually depending on the complexity of your operation, but a single missed deduction or late filing penalty often exceeds that cost. If you operate multiple properties or have high income, the investment becomes even more critical because the tax code offers more deductions and strategies that require professional guidance to implement correctly.

Automate Lodging Tax Filing Across Multiple Jurisdictions

Services like Avalara MyLodgeTax handle the mechanical work of filing lodging tax returns across multiple jurisdictions, removing the burden of tracking different local filing deadlines and rates. This automation reduces errors and ensures you never miss a filing deadline, which is especially valuable if your property operates in a city like Minneapolis where local lodging taxes are substantial and filing requirements are strict. The combination of proper record-keeping systems and professional tax guidance transforms vacation rental taxation from a source of anxiety into a manageable compliance process.

Final Thoughts

Vacation rental taxes in Minnesota operate across multiple layers-federal income tax, state income tax, lodging taxes, and local compliance requirements-and owners who address each layer avoid penalties and capture available deductions. Your federal tax bill depends on reporting gross income correctly and claiming every legitimate deduction from mortgage interest to depreciation, while Minnesota state income tax adds another 5.35% to 9.85% on your net profit. Lodging taxes that you collect from guests must reach the Minnesota Department of Revenue on strict deadlines, or penalties compound quickly.

The most common mistakes occur when owners underestimate their tax complexity and mix personal and rental finances, assume platforms handle all taxes (leaving local lodging tax gaps unfilled), fail to track material participation hours (costing thousands in unnecessary self-employment taxes), or skip zero-dollar returns during slow months. Separation protects you: maintain separate accounts, separate records, and separate documentation of every transaction and activity hour. Hire a tax professional who understands vacation rental operations in Minnesota, not just general accounting, and automate lodging tax filing if you operate across multiple jurisdictions.

If managing vacation rental taxes feels overwhelming alongside property operations, professional management can simplify your situation. We at Up North Property Management handle marketing, bookings, cleaning, and maintenance for vacation rentals across Northern Minnesota, which frees you to focus on tax compliance and financial planning-visit Up North Property Management to explore how we can help. Start now by opening a dedicated rental account, gathering last year’s records, and scheduling a consultation with a tax professional who specializes in vacation rentals.