Most cabin owners think their homeowners insurance covers their property. It doesn’t.

We at Up North Property Management see this mistake constantly. Cabins face unique risks-from seasonal vacancy gaps to water damage exclusions-that standard policies simply don’t address. The right cabin insurance protects your investment and keeps you from facing catastrophic losses when something goes wrong.

What Cabin Insurance Actually Covers

Standard cabin insurance policies protect three core areas, and understanding what falls under each one matters far more than most owners realize. The dwelling coverage pays to repair or rebuild the cabin structure itself, including the roof, walls, and foundation. Personal property coverage protects your belongings inside the cabin, from furniture to kitchen equipment.

Liability coverage shields you financially if a guest gets injured on your property and sues, covering medical bills and legal defense costs. Fire, theft, vandalism, windstorms, hail, lightning, and water damage from storms all typically fall under standard coverage. However, the word typically is dangerous here. Your specific policy only covers perils explicitly listed in the contract, so reading the actual wording matters more than trusting assumptions.

Water Damage Requires Serious Attention

Water damage represents the leading cabin insurance claim by far, and it’s also one of the easiest losses to prevent. A burst pipe from freezing temperatures, a roof leak during heavy snow, or foundation seepage from spring melt can cost thousands in repairs and mold remediation. Most owners fall into a trap when they leave the cabin closed during winter without shutting off the main water supply. If a pipe freezes and ruptures while you’re away for weeks, your standard policy might deny coverage if it considers the loss preventable through basic maintenance. Shut off the main water supply before closing the cabin seasonally or before leaving for extended periods. Keep your roof in good repair, clear gutters and downspouts of debris, and maintain proper drainage around the foundation as practical first steps. If your cabin sits in a region with heavy snow, clearing significant snow accumulation one to three times per season can help prevent roof collapse from the weight.

Liability Protection and Guest Safety

Liability coverage protects you when someone gets hurt at your cabin and decides to sue. This is not theoretical. The average homeowners policy includes around $100,000 to $300,000 in liability protection, which sounds adequate until a guest breaks a leg on your deck and racks up $50,000 in medical bills plus demands $200,000 for pain and suffering. For cabins that host guests regularly, especially rental properties, standard homeowners liability limits fall short. Vacation rental-specific policies typically offer higher limits, often starting around $1 million, which aligns with actual exposure when strangers visit your property. Liability coverage also pays your legal defense costs if someone sues, which can easily exceed $10,000 to $20,000 even if you ultimately win the case. Proactive maintenance reduces your actual liability risk significantly. Inspect decks and balconies annually for rot or structural weakness, arrange professional chimney sweeping for wood-burning fireplaces, and remove outdoor furniture before heavy wind events to lower the chance of an incident that triggers a claim. Document this maintenance with a digital log to strengthen your legal position if a guest later claims negligence.

What Gaps Appear in Most Policies

Most cabin owners discover coverage gaps only after a loss occurs, which is far too late. Seasonal vacancy periods create exposure that standard policies don’t address adequately. Extended absences (weeks or months without occupancy) can void coverage or require special seasonal riders. High-value items like art, jewelry, or recreational equipment often hit coverage limits quickly, leaving significant out-of-pocket exposure. Flooding and earthquakes fall outside standard cabin policies entirely, requiring separate specialized coverage. Your policy exclusions determine what you actually own versus what you think you own, so the next step involves comparing multiple quotes to identify which gaps matter most for your specific property.

Where Cabin Insurance Actually Fails

Vacancy Gaps That Leave You Exposed

Extended vacancy periods expose a critical weakness in standard cabin policies that most owners don’t discover until after a loss strikes. If your cabin sits unoccupied for more than 30 to 60 days-depending on your insurer-your coverage may be suspended or require a special seasonal rider at additional cost. This gap matters enormously because cabins are vacant by nature. You’re not there year-round, and winter closures stretch for months.

Insurance companies view vacant properties as higher risk for theft, vandalism, and undetected water damage. They either exclude coverage during those periods or charge extra to maintain it. Contact your insurer before the season ends to confirm whether your policy includes seasonal vacancy coverage and what specific conditions apply. Some carriers require someone to inspect the cabin every 7 to 14 days during vacant periods, while others simply charge a higher premium. If your current policy doesn’t cover extended vacancy adequately, seasonal cabin insurance exists specifically for this problem, though it typically costs between a few hundred and just over a thousand dollars annually depending on cabin size and location.

Personal Property Coverage Limits Fall Short

High-value items represent a separate but equally damaging gap in standard policies. Personal property coverage under standard cabin insurance caps at $5,000 to $10,000 for individual items like jewelry, art, or electronics. A collection of nice furniture, kitchen equipment, or recreational gear quickly exceeds your protection. Separate scheduled personal property riders can extend coverage for specific valuable items, but you must list them individually and provide proof of value. This extra step takes time, yet it prevents catastrophic losses when theft or fire strikes.

Flooding: The Coverage Gap That Costs the Most

Flooding stands apart entirely because standard cabin insurance excludes it completely. Whether a river overflows, heavy rain causes foundation seepage, or a plumbing failure leads to water accumulation, flooding is not covered. According to Aviva, water damage claims represent the leading cabin insurance claim overall, yet most owners don’t realize that weather-related flooding requires a separate flood insurance policy through the National Flood Insurance Program or private carriers. If your cabin sits in a flood zone or near water, this is not optional-it’s the single most expensive mistake cabin owners make. The same applies to earthquake damage in seismic regions.

Shutting off the main water supply before leaving for weeks, clearing gutters and downspouts, and maintaining proper foundation drainage reduce preventable water losses. However, only a separate flood policy covers actual flooding events that fall outside your control. This distinction matters because prevention protects against some losses but not all of them. Your next step involves identifying which specific gaps pose the greatest risk to your property and your finances.

Finding the Right Cabin Insurance Without Overpaying

Calculate Your Cabin’s True Replacement Value

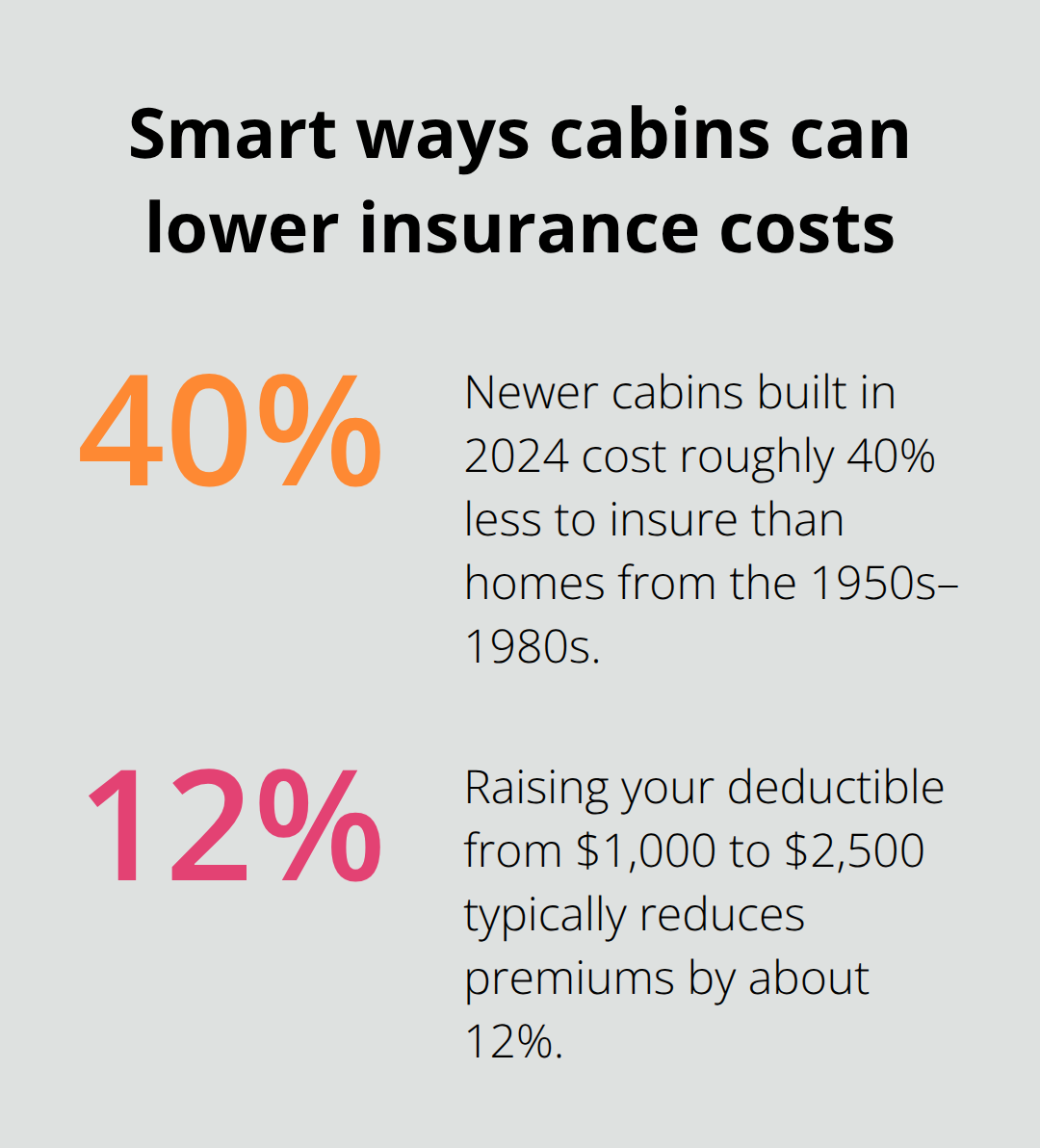

Start by calculating your cabin’s actual replacement value, not what you think it’s worth. This number determines your dwelling coverage limit and directly impacts your premium. A cabin that costs $150,000 to rebuild requires different coverage than one that costs $400,000. Dwelling coverage amounts drive premium costs significantly: a $200,000 dwelling limit averages around $1,555 annually, while $400,000 in coverage runs approximately $2,655 per year. Your cabin’s construction type, age, and materials matter enormously. Newer cabins built in 2024 cost roughly 40% less to insure than homes built in the 1950s and 1980s, according to the same data.

Identify Your Specific Risk Factors

Next, identify your specific risk factors honestly. Does your cabin sit in a wildfire-prone forest area? Is it in a flood zone? Does it experience heavy snow loads or strong winds? Does it sit near a fire station or in an area with higher crime rates? Each factor influences both coverage needs and premium costs. A cabin in southwestern Alberta faces substantially higher wind damage risk and should prioritize wind-resistant roofing or heavier materials like tile or rubber. A cabin near a river needs separate flood insurance through the National Flood Insurance Program, not just standard coverage. Document these risks before contacting insurers because they’ll ask anyway, and your answers determine which carriers will even quote you.

Compare Quotes From Multiple Carriers

Comparison shopping across at least three different insurers is non-negotiable, and this is where most cabin owners fail. NerdWallet’s data shows significant variation between carriers: Travelers averages $2,055 annually, State Farm around $2,185, Allstate approximately $2,380, and Farmers roughly $2,600 for similar coverage.

An independent insurance agent or broker can gather quotes from multiple carriers simultaneously, saving you hours of phone calls and ensuring you compare identical coverage limits and deductibles across all quotes.

Review Exclusions and Coverage Details

When reviewing quotes, focus on what’s actually excluded, not just the premium price. Ask explicitly whether seasonal vacancy periods coverage requirements apply and what notification requirements apply if you’re absent for 30, 60, or 90 days. Most standard policies contain vacancy clauses that void protection after this period, which leaves you exposed to theft, vandalism, and weather damage. Confirm whether your policy includes personal property coverage limits for high-value items and whether you need scheduled riders for jewelry, art, or recreational equipment. Ask about liability limits and whether they match vacation rental exposure if you rent the cabin to guests. Request clarification on water damage coverage, particularly for frozen pipes and weather-related seepage, versus flooding exclusions that require separate insurance.

Optimize Your Deductible and Discounts

Raising your deductible from $1,000 to $2,500 typically reduces premiums by approximately 12%, according to NerdWallet, but only if you have emergency savings available to cover that amount if a loss occurs. Finally, ask about available discounts: multi-policy bundling with your primary homeowners policy can improve eligibility and lower total premiums, while safety devices like alarms, cameras, and smart detectors may qualify for reductions. Some insurers offer annual payment discounts compared to monthly installments. Don’t skip this step because it directly affects your bottom line.

Final Thoughts

Adequate cabin insurance protects your investment from the financial devastation that follows water damage, theft, liability claims, or natural disasters. Without proper coverage, a single incident costs tens of thousands in repairs, legal fees, and lost income if your cabin becomes uninhabitable. The gaps throughout this guide-seasonal vacancy exclusions, personal property limits, and flooding-represent real exposures that affect real cabin owners every year.

Contact your current insurer and confirm exactly what your policy covers during extended vacancy periods. Request a written summary of your dwelling coverage limit, personal property limits, liability protection, and all exclusions. Calculate your cabin’s true replacement value and compare it against your current dwelling coverage; if the numbers don’t align, you’re underinsured.

Reach out to at least three different carriers for quotes on policies that match your actual replacement value and risk profile. An independent insurance agent can handle this comparison work for you, saving time and ensuring you evaluate identical coverage across all quotes. Up North Property Management handles maintenance and guest screening, reducing liability risk while ensuring your property stays in top condition.